Receiving your salary, paying bills or rent… Opening a Swiss bank account will certainly make all your financial arrangements (salaries, bills, rent) much easier once you’re there! Plan ahead by finding out about the banks and the various options available to you. In this article, b-sharpe, your currency exchange partner, explains everything you need to know about opening a bank account and Swiss banks.

Opening a bank account in Switzerland: a quick and easy process

Opening a bank account in Switzerland is easier than you might think. For French expats or cross-border workers, the process is usually quick. What are the requirements for opening an account in Switzerland? What supporting documents are required? Find out below.

Good to know: some Swiss banks, such as UBS and Credit Suisse, have branches in France where you can open a bank account.

How to open a bank account in Switzerland

When you open your new bank account in Switzerland, you will, of course, need to provide certain documents to your new bank. Whilst the required documents may vary from bank to bank, you will always be asked to provide:

- Proof of identity, such as a passport or national identity card;

- Proof of address (an electricity, internet or water bill, etc.)

- Bank statements;

- Proof of employment in Switzerland;

- Proof of income.

Is it possible for a French citizen to open a bank account in Switzerland?

Can I open a bank account in Switzerland if I am a French national? Absolutely. It is legal for French nationals to open a bank account in Switzerland. However, you are required to declare any bank accounts held abroad to the French tax authorities and to include them in your annual tax return.

Can you open a bank account in Switzerland if you are a non-resident?

Do you live in France or elsewhere abroad, outside Switzerland, and wish to open a bank account in Switzerland? It is possible! However, some banks may ask you to make a substantial deposit, or require you to provide proof of income to demonstrate your creditworthiness. Furthermore, the tax authorities in your country of residence must be notified of the opening of a foreign bank account. Your Swiss bank will therefore have to send a list of all transactions carried out to the tax authorities in your country every year.

Is it possible to open an account online?

Good to know: you can open a bank account in Switzerland online or remotely. However, you will need to submit all the necessary documents online or by post, depending on the option you choose.

Everything you need to know about banks in Switzerland

As you’re no doubt aware, Switzerland is the banking capital of the world! There’s therefore a wide range of banking options available… From traditional players such as PostFinance, Credit Suisse and UBS to neobanks like Swissquote and Yuh… How do you make sense of it all? Here are the key factors to consider when choosing your banking partner, before opening an account in Switzerland.

The advantages of Swiss banks

Why open a bank account in Switzerland? The Swiss banking system is renowned worldwide… Swiss banks offer a number of advantages:

- Greater security for funds: the Swiss financial landscape is one of the most heavily regulated in the world. Financial regulators impose strict rules on banks, particularly regarding the protection of funds and banking secrecy. Indeed, national law stipulates that banks may under no circumstances disclose their clients’ financial information.

- A world-renowned financial system: the Swiss financial centre offers banking services of the highest standard. This applies not only to traditional banks but also to private banks specialising in wealth management.

- Economic stability at national level: as you know, Switzerland is an economically stable country. Wages and the standard of living are very favourable. The Swiss minimum wage is among the highest in the world. The pension system (Swiss LPP) is also robust. Banks therefore benefit from a favourable political and economic climate.

Opening a bank account in Switzerland: how to choose the right bank?

Which is the best bank to open an account with in Switzerland? It’s hard to say, given the sheer number of banks in the country! They offer a range of services and tailor their offerings to their customers’ needs. Switzerland is a federal and multilingual state. As such, there are several types of banking institutions:

- Universal banks, which operate nationwide;

- Local banks operating at cantonal level;

- Co-operative banks;

- Private banks, which specialise in wealth management;

- Online banks (neobanks).

Are you looking to open a current account (also known as a salary account) in Switzerland? If so, universal or cantonal banks will undoubtedly be the most suitable option. Finally, there is another option available to you: online banks. Flexible and paperless, they often charge lower bank fees.

Are you a cross-border worker living in France? You should know that some Swiss banks offer so-called “cross-border” accounts, specifically designed for this particular status! These accounts offer few options, as they are designed solely to receive your salary and transfer it to a French account in euros. This is an advantageous and less expensive solution for having your salary paid in Swiss francs (CHF). However, you should check with your employer before opening a cross-border account with a French bank: some Swiss employers require a Swiss IBAN for salary payments.

The issue of bank charges

What are the costs associated with debit and credit cards? Bank charges in Switzerland are relatively high. This is an important point to bear in mind before opening a bank account in Switzerland. Be sure to compare the offers from different banks.

The amount of the monthly account maintenance fee varies from bank to bank. On average, it amounts to 20 Swiss francs for a current account that includes a debit card. The more features and services your bank account includes, the higher the fees will be. Withdrawals from ATMs (also known as Bancomats in Switzerland) belonging to your chosen bank are generally free of charge. Some banks charge a fee if you withdraw from a Bancomat belonging to another bank. International transfers or withdrawals abroad may also be subject to charges. The same applies to overdraft charges.

Finally, if you travel regularly within the eurozone or are a cross-border worker, consider choosing a bank that allows you to withdraw cash in both euros and Swiss francs. However, you can still exchange currencies online easily and at preferential rates using a euro-to-Swiss franc converter such as b-sharpe.

FAQ

Are you a cross-border worker or an expat looking to open a bank account in Switzerland? b-sharpe has all the answers to your questions about opening a bank account in Switzerland.

What are the requirements for opening a bank account in Switzerland?

Opening a bank account in Switzerland is a very straightforward process. This applies even to non-residents. What are the requirements? You must be of legal age, provide a work permit (or G permit), proof of identity and proof of address, as well as a statement explaining the source of your funds. Please note that US citizens may only open a Swiss bank account under certain conditions.

Can I open a business bank account in Switzerland as a French national?

Technically, yes. But that means your business must be registered in Switzerland. Switzerland offers many advantages for entrepreneurs, including a simplified administrative framework and faster processing times compared to France. However, certain eligibility criteria must be met to set up a business as a foreign national. Therefore, it is essential to hold a residence permit (type B or G) or to partner with a Swiss resident in order to legally establish a company in the country.

Setting up a business, and therefore opening a business bank account in Switzerland, can be more complicated for non-Swiss residents due to strict compliance requirements. Swiss banks scrutinise the source of funds and the business sector very closely. It is advisable to seek professional assistance to streamline this process and ensure compliance with Swiss banking regulations.

Can a French citizen open a bank account in Switzerland?

Yes, a French national can certainly open a bank account in Switzerland. However, the situation may vary depending on their residency status (residence permit, cross-border worker status, non-resident). Please contact a Swiss bank for further information.

Can you open a bank account in Switzerland for free?

Yes and no. Traditional Swiss banks charge account maintenance fees, so it is not possible to open an account with them for free. However, some online banks (or neobanks) based in Switzerland offer free account openings. You will then have a Swiss IBAN in CH. Some fees or services will subsequently incur a charge. Their services are provided entirely online. Please note: make sure you check carefully beforehand, as these banks are not always compatible with receiving your Swiss salary. Some employers require accounts with traditional banks. However, neobanks are still useful for holding a secondary account.

How can I convert my Swiss francs into euros without a Swiss bank account?

If you live or work between France and Switzerland, you will no doubt need to regularly convert currency between euros and Swiss francs, and vice versa. To exchange your currency, there are several options available to you, such as traditional banks or bureaux de change, financial institutions specialising in foreign currency conversion. It is also possible to exchange your euros or Swiss francs, as well as many other currencies, directly online. b-sharpe offers an online currency converter, updated in real time, for all your transactions. Take advantage of competitive rates to carry out your online currency exchanges in over 20 currencies: Swiss francs to euros, Swiss francs to pounds sterling, or even dollars to euros…

b-sharpe allows you to benefit from a very competitive exchange rate compared to traditional providers. The rate offered for EUR-CHF or CHF-EUR conversions is therefore significantly lower than that of a traditional bank. Every transaction is carried out with complete transparency. The fees applied to each transaction are clearly stated before each conversion. b-sharpe guarantees its users transparency and security.

To live in Switzerland, opening a local bank account is essential. But to help you settle in Switzerland and manage your finances, you will also need a currency converter. b-sharpe supports you in all your transactions, enabling you to exchange currencies online easily, reliably and transparently.

Hidden bank charges charged to private individuals – what you need to know!Tax regulations, types of banking transactions, the commercial policies of certain banks… Few people realise it, but there are many factors that can cause the bank charges levied on individuals to vary (and therefore increase).

It is therefore best to keep yourself informed about the main bank charges (which can sometimes be hard to spot), as you might unfortunately only realise what they are once they have been debited. As the saying goes: ‘forewarned is forearmed’!

Rather than compiling a tedious and incomplete list of Swiss bank charges, this article aims to help you gain a clearer understanding of certain practices that are far from being as transparent or advantageous as banks would have you believe.

Few individuals actually compare the costs associated with banking services

According to a study on currency exchange in Switzerland carried out in 2016 – which remains largely relevant today – of the 72% of individuals who transfer half or more of their salary to France, nearly 59% regard the cost of currency exchange as a key factor when choosing their bank.

However, very few retail customers actually compare exchange rates, spreads and direct or indirect bank charges… According to the same study, 35% of retail customers surveyed have never compared the charges for different services, and only 11% do so before each transfer.

Yet the potential savings are huge: with average fees of between 3% and 3.8% when using a bank, a private individual earning a salary of CHF 5,000 would save between €900 and €1,200 in exchange fees per year by using an online currency exchange service such as b-sharpe, rather than their traditional bank.

Costs associated with having a bank account abroad

In recent years, a great many individuals have noticed a significant rise in their bank charges; a rise that affects virtually all areas of expenditure.

For regulatory and supervisory reasons, the automation of the exchange of tax-related information between Switzerland and France has caused a sharp rise in the administrative costs associated with account management.

Charges such as ‘fees for non-Swiss bank accounts’, ‘non-eurozone bank charges’ and ‘tax statement fees’ have thus been levied on a massive scale. Whilst there is no question that these charges are justified, they are, above all, highly volatile and vary from one institution to another.

Do you need to manage a multi-currency personal budget? Discover our 6 tips for managing your international income and expenditure!

Following the introduction of the exchange of tax information between Switzerland and the European Union, banks have had to deal with additional administrative and regulatory requirements for their clients who are resident abroad.

Most Swiss banks therefore charge additional fees to customers domiciled outside Switzerland (including Swiss nationals living abroad). This means that, in addition to the ‘standard’ account maintenance fees and bank card fees (for debit or credit cards), there are also direct debit fees.

Once again, although the banking sector is highly regulated, particularly by the Swiss Financial Market Supervisory Authority (FINMA), each bank remains free to set its own management fees and margins. It is entirely up to them to make these clear to all their customers…

Example: For some banks or banking institutions in Switzerland, expect to pay between 300 and 480 Swiss francs in tax each year for each Swiss account (for customers resident abroad).

In this specific case, taxes are levied on each client, regardless of their wealth or country of residence. However, it is important to note that these taxes are calculated per account based on payment transactions, rather than per banking relationship.

In addition, the fees associated with a salary account or current account also depend on:

- the amount;

- whether or not they have a savings account;

- whether or not you have a 2nd or 3rd pillar pension scheme;

- whether or not one has assets.

Please note: Once a certain threshold is reached (which varies depending on the bank), the fees are reduced or even waived entirely.

Inclusive fees for individuals working in Switzerland

Although we have tried, like many researchers before us, to compare the fees for Swiss franc bank accounts, it seems that all the players in the sector are working very hard to make their offerings difficult to compare!

These are all the more difficult to compare given that some institutions use:

- all-inclusive packages;

- loyalty schemes;

- plans with the first year free…

In fact, to best identify the various bank charges you may be incurring without realising it, please pay close attention to the following:

- collaborations between banks and insurance companies,

- to loyalty schemes offering discounts,

- the costs associated with the various payment cards,

- the costs associated with international bank transfers…

Bear in mind that these offers are available for a limited time only. Not to mention that switching banks is often so complicated that many of us would prefer to stay put. As you can see, for individuals working in Switzerland, the fees – far from being free – are in fact ‘built in’.

The margin on foreign exchange transactions

As you know, currency exchange transactions aren’t free. Yet some financial institutions still rely on slogans worthy of telecoms operators, promising that these transactions are free!

Monito, a website that compares and reviews money transfer services, highlighted the practices of banking operators, which use carefully crafted and somewhat misleading slogans such as: “free money transfer home”, “transfers to France with no fees, no commission”…

However, exchange fees, or even commissions, are systematically applied to the official interbank exchange rate; these are generally visible and clearly stated.

Need to make a SEPA transfer? Discover 3 ways to avoid paying receiving charges!

Are online banks and neo-banks more transparent?

Competition does not necessarily mean transparency, even following the arrival of online-only banks – these new generalist banking players, which operate entirely online and are referred to as ‘neobanks’.

Are ‘100% free’ banking offers really as good as they seem? Whilst all basic banking services – such as withdrawals, payments and online account access – are advertised as completely free, some of these services actually come with a charge when you look more closely.

What’s more, special services come at a high price: requests for duplicate documents or PIN codes can quickly drive up the bill. Similarly, inactivity can prove very costly with an online bank account, as fees are charged automatically and progressively if the customer does not carry out enough transactions each month.

You now know all about the bank charges (some more justified than others) that many people pay without ever realising it… We hope this article will help you manage your costs as effectively as possible, making it easier to manage your budget.

Need to pay your bills in foreign currencies? b-sharpe lets you get very competitive rates in complete security!

BVR, BVRB, SBVR: what are the differences?Did you know that payment slips have been used in Switzerland since 1906? Back then, they were green, had three sections, and were used by the postal service.

More than a century later, the first Swiss QR invoices have arrived on the scene and are set to replace the old orange and red payment slips. But how well do you know these payment slips and the features that set them apart?

What is a payment slip?

A payment slip is a document used in Switzerland to make a payment (in cash or by bank or postal transfer) into a bank account.

This payment method, offered by PostFinance (the Swiss Post’s financial arm), has been in use in Switzerland since 1906 in various forms that have evolved over time.

In recent years, seven different types of payment slips have been included with the majority of invoices issued in Switzerland and are used by both individuals and businesses.

Payment slips do indeed offer certain advantages. Recipients receive all the information they need to make a payment in a single document. What’s more, when a printed payment slip is attached to an invoice, the recipient does not need to fill in all this information by hand.

Please note: As QR invoices are gradually replacing payment slips, b-sharpe no longer supports these older payment methods, but instead offers you the most modern, efficient and cost-effective payment solutions.

What are the differences between the red and orange payment slips?

Of the seven types of payment slips commonly used in Switzerland, two main categories stand out: red payment slips and orange payment slips.

Also known as a “payment slip without a reference number”, the red payment slip (BV) allows you to make a direct payment into a recipient’s bank account. It is usually filled in by hand.

Also known as a “payment slip with a reference number”, the orange payment slip (BVR) allows for automated payments to be made to a recipient’s account, as it is pre-filled by the invoice issuer.

In addition to this key distinction, the red and orange payment slips have a number of differences.

Unlike the red payment slips, the orange payment slips:

- have a reference number and are assigned to debtors on a one-to-one basis;

- enable the automation of payment reconciliation;

- enable you to send reminders easily and automatically.

Unlike the orange payment slips, the red payment slips:

- can be processed entirely by hand;

- display an additional information field where necessary;

- are more expensive, as they involve cash payment fees.

What is a BVR?

Definition

An orange payment slip with a reference number (BVR) is a document used for automated billing and collection.

As the name suggests, this statement features a printed reference number that makes the billing process easier and more secure.

In fact, the reference number on each payment slip can be decoded by specialised software, which automatically records the corresponding payment entry, either in Swiss francs or in euros.

This is why this processing system is used by many companies, particularly when they are handling large financial transactions.

How the reference number works

The length of a BVR reference number varies depending on the bank accounts involved in the transaction. The number can therefore consist of between 15 and 26 digits and can be changed at will, with the exception of the very last digit, which acts as a “check digit”.

The other digits can be easily generated using free software and form the code corresponding to the final reference number. In particular, they refer to:

- the amount of the invoice;

- the invoice number;

- the bank account number;

- to the BVR participant number.

Good to know: There are two distinct types of orange payment slips: BVRs and BVR+s (which allow you to enter the amount to be paid yourself).

What is a BVRB?

A Bank Reference Payment Slip (BVRB) is a variant of the BVR designed for start-ups and small businesses that do not have the necessary infrastructure to set up automated processing of financial transactions. BVRB slips can be ordered pre-printed from banks.

With this form, identification is carried out either via:

- bank account number;

- the customer number contained in the reference number;

- of the bank ID.

Please note: BVRB payment slips do not allow for automatic reconciliation of incoming payments with the company’s accounts.

What is an SBVR?

A Bank Reference Payment Slip System (SBVR) is a variant of the BVR designed for businesses equipped with software capable of processing BVRs. Typically supplied directly by the relevant banks, this specialised software enables them to automate their accounting processes on an ongoing basis.

What are the differences between BVR, BVRB and SBVR?

These three designations therefore refer to three different types of orange payment slips. Unlike red payment slips, these three slips feature reference numbers to enable the billing process to be automated.

Here are the differences between these three designations:

- BVR refers to a payment slip with a reference number that simplifies and automates invoicing;

- BVRB refers to a bank-referenced payment slip designed for small businesses, which can be printed with an invoice number from the bank or post office;

- SBVR refers to a bank-referenced payment slip system designed for businesses that use BVR processing software.

Red and orange payment slips have been used for years by Swiss businesses and individuals in their invoicing, payment and collection processes. In particular, they enable them to simplify and automate these procedures, which can be very time-consuming when carried out manually.

Orange payment slips come in three distinct formats (BVR, BVRB and SBVR), each corresponding to different structures, activities and procedures, and offering options tailored specifically to the profiles of issuers and recipients.

Find out more about the processing times for a bank transactionWhy is there a delay between sending a bank transfer and receiving the payment?

First of all, we need to understand what a financial transaction involves in order to understand why it cannot be instantaneous.

A financial transaction is, first and foremost, an exchange of information between two institutions holding funds on behalf of third parties in order to carry out a transfer. It is a process that must be reliable, unique, secure and comprehensive. The consequences of an error can be particularly serious.

What are the different types of bank transfer and the associated processing times?

Financial institutions generally classify transactions into four main types, each of which is further divided into two categories.

We therefore have:

- Account-to-account transfers: These are transfers between two accounts held by the same account holder at the same bank. These transfers are instantaneous, regardless of the value date, provided that the account being debited has sufficient funds.

- Domestic transfers: these are transfers between two accounts in the same country and in the same currency, held at two different banks. These transfers take between 1 and 3 working days. In most cases, the funds are credited to the recipient’s account the morning after the transfer is initiated.

Domestic transfers between two accounts held at the same bank are usually completed within a few minutes. - SEPA transfers: these are European payments denominated in euros, initiated by a bank authorised to carry out this type of transaction and received by a bank that accepts SEPA (essentially all European banks). The processing time is the same as for a domestic transfer. It should not take more than three working days.

- International bank transfers: in this case, the transfer is made between two banks located in different countries that have not signed any specific agreement, and the currencies involved may not necessarily be the same. This can take between 1 and 5 working days.

These payments include:

- Instant or Express transfers: often charged by the bank when made in the afternoon, the transfer is processed immediately. Please note that an express transfer in euros falls outside the scope of the SEPA agreement.

One of the benefits of using instant transfers is that they allow transactions to be completed on the same working day for domestic transfers. - Scheduled transfers: this is the most common use of a transfer; the instruction is carried out on a specific date, often the day after the request is made, but this can be set for a date of the sender’s choosing.

My transaction isn’t going through on time. Why is that?

Assuming that your account has sufficient funds and that the payment has been successfully debited, there are many reasons why the funds might not have been credited yet. We will list the most common reasons here, but this list is by no means exhaustive.

The most common error concerns your payee’s bank details. This may relate to your payee’s name, address or IBAN. If there is no perfect match between these three details, the receiving bank is entitled to reject the funds. If the funds are rejected, the payment will be returned within 2–3 working days.

Please note that charges may apply if funds are returned, particularly in the case of international transfers.

The processing time may also be affected by financial institutions’ internal checks. During a financial transaction, regardless of the amount, financial institutions may carry out a number of checks. Until these checks have been approved, the transaction remains pending.

The main reasons for these checks are: the unusual amount involved in the transaction, the new source of the funds, the country of origin, the name of the beneficiary, or the country of destination.

If there is a hold on the transaction, banks are entitled to request clarification and further information. This may take up to a week.

Finally, the involvement of an intermediary bank can affect the processing time of your transaction. This is particularly the case for payments denominated in US dollars. In such cases, a bank acts as an intermediary between the sender’s bank and the final recipient. This is unavoidable, but some banks are slower than others in processing these transactions, which can delay your transactions by several days.

What can be done to minimise the risk of delays?

Sharing information with the institutions involved in the transaction is key to keeping the processing time to a minimum. When you carry out a financial transaction that falls outside the usual scope, your bank is required to carry out checks.

If your advisor has been notified of the transaction and has all the information required to approve it, they will process it as soon as it is received. Among other things, they will be able to ask you any necessary questions before the transaction goes ahead, thereby avoiding any hold-ups by addressing potential issues one by one. For example, they can inform their colleagues if they are absent or answer questions from the counterparty without having to ask you.

If he does not have the information to hand, he should get in touch with you, which he will do as soon as he has a moment. This could be within five minutes or within two days.

To minimise delays, we therefore recommend that you send a message with supporting documentation or an explanation to your bank advisor as soon as you carry out or anticipate a transaction that falls outside your usual banking activities (first Swiss salary, property transaction, management of your 2nd pillar pension, etc.).

So what impact does b-sharpe have on transaction times?

b-sharpe is a foreign exchange broker and, as such, a financial intermediary. We are therefore subject to the same regulations as banking institutions.

We do our utmost to minimise the processing time for your transaction. Transactions processed before midday are settled on the same day for all transactions in CHF and EUR. We process your transactions within a maximum of 12 working hours from the time we receive your funds to the time we issue the payment of the equivalent amount.

However, we are still subject to bank processing times, so the time taken may vary between 1 and 3 days, even though the payment is processed within minutes of receiving your funds.

Furthermore, as an intermediary, we are entitled to ask you for further information regarding the financial background of your transactions. If we do not receive a response from you, the transaction will be put on hold on our end.

Using b-sharpe therefore has very little impact on the processing time of a standard banking transaction, whilst allowing you to benefit from particularly favourable exchange rates.

Generally, our customers are credited within 24 hours of their transaction being processed.

BEN, SHARE, OUR: International payment optionsWhich payments are affected?

This article will examine the payment framework applicable to all international financial transactions outside the SEPA area. Indeed, this framework entails a cost structure that is directly determined by the directives and specific characteristics of this type of transaction.

These various schemes therefore apply to all transfers outside the SEPA framework, including express payments in euros, which by definition fall outside the SEPA framework.

Why are there charges on international transfers?

A banking transaction involves more than just transferring funds from Bank A to Bank B; it is a secure and reliable transfer of information between two private entities, often operating in different countries, which may require the involvement of several other entities in order to reach its destination.

As part of the process of setting up this payment, there are fees associated with the processing carried out by the financial institutions involved in the transaction. These fees can be substantial and must be taken into account before any payment is made.

These charges generally consist of administration and processing fees and, unfortunately, can very rarely be predicted in advance of a transaction. To manage these charges, banks and financial institutions have introduced standardised payment and cost schemes. These schemes determine whether the sender or the recipient is responsible for the transfer charges.

These administration and payment fees usually range from a few francs to several dozen francs for a transfer to the United States, for example.

There are currently three main fee structures: OUR, BEN and SHA. Each of these three structures has its own specific features and advantages.

The three cost models:

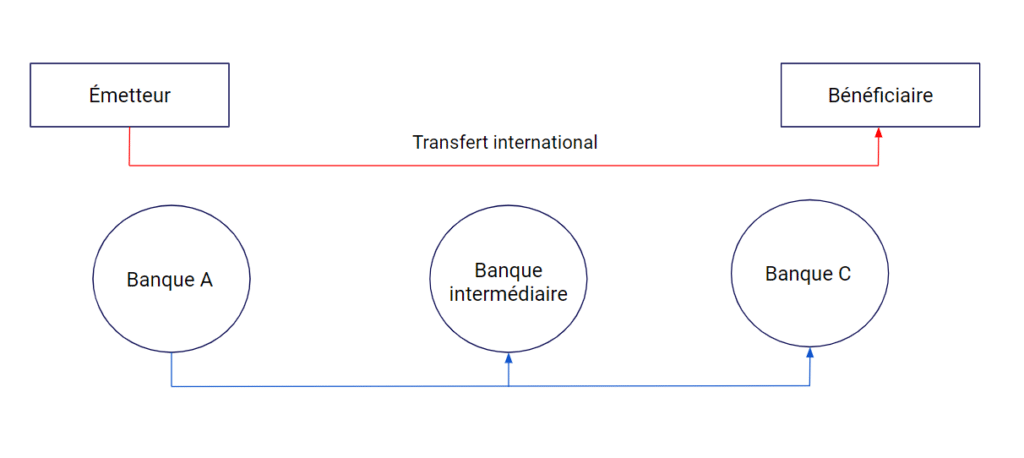

To explain the conditions for each of these three options, we will refer back to the diagram at the top of the page.

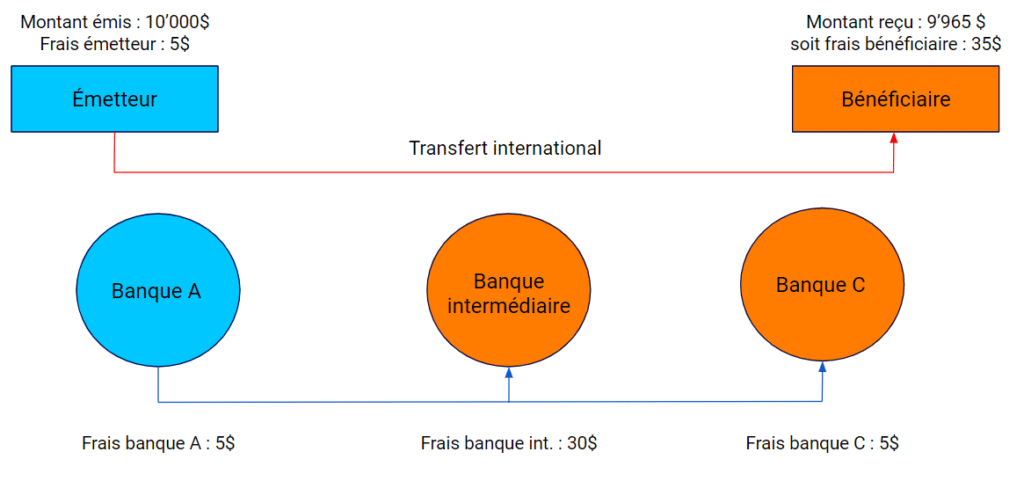

SHA: Share or cost-sharing

This is the default scheme used when processing a financial transaction. This scheme allocates the charges between the issuer and the beneficiary. The allocation is as follows:

- The costs relating to the issuer’s bank (Bank A) are to be borne by the issuer.

- Any charges relating to the intermediary bank and the beneficiary’s bank (Bank C) are to be borne by the beneficiary.

Please note that when making a payment using this method, the recipient is likely to receive a lower amount than the amount you have sent. It is therefore important to specify the method used when settling the invoice.

This is particularly important when paying an invoice to China or the United States, as intermediary banks will inevitably charge for their services.

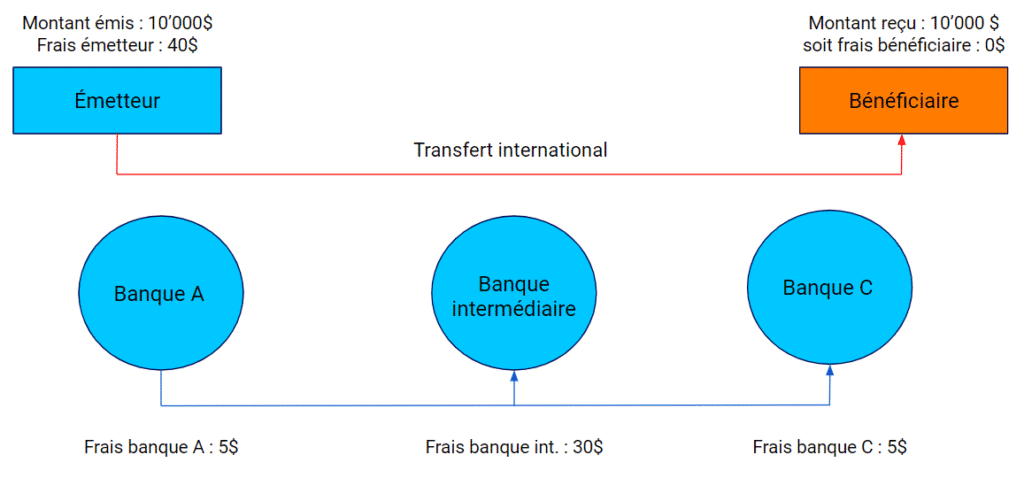

OUR: Our or costs to be borne by the issuer

This method is much more specific and less common, but it ensures that the recipient receives the full amount sent by the sender. In this case, the sender covers all the costs associated with the transaction; consequently, the recipient does not have to pay anything and receives the full amount sent.

As the costs are unpredictable, financial institutions tend to charge a flat fee to cover all expenses. This usually costs around thirty francs and is specifically intended for business use.

As this form is not used by default, please do not hesitate to ask your financial advisor if it is the one you need.

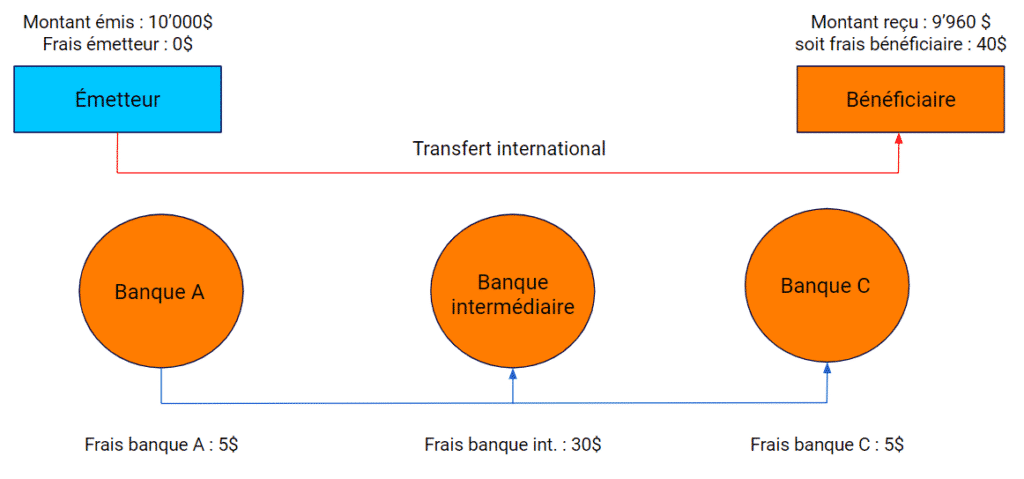

BEN: Beneficiary or costs to be borne by the beneficiary

This method is rarely used; it is often costly for the beneficiary and therefore does not provide a solution to the issues surrounding the payment of an invoice. However, it can be useful when it is impossible to determine the cost of a transaction with certainty, or in the context of certain contracts.

In this scenario, all costs associated with the transaction are borne by the recipient. Consequently, the sender knows exactly how much will be debited from their account, whereas the recipient can be certain that they will receive an amount lower than the amount sent. This is useful when no agreement has been signed and you wish to pay a specific amount, regardless of the amount received by the recipient.

What about b-sharpe, then?

As part of our service enabling you to pay your international suppliers directly, b-sharpe is able to offer you these three pricing options.

Like other financial institutions, we use the SHA scheme by default and free of charge.

At your request, and when processing your invoice payment, we can use the OUR scheme and therefore cover the full cost of the transfer. This scheme costs CHF 28.

Although the BEN scheme is less commonly used, it remains available and is completely free of charge.

Conclusion

The cost structure is therefore a key factor in the signing and management of a commercial contract involving international financial transactions. Each of these three solutions is sound and has its own advantages and disadvantages. As part of our business, we offer these three methods depending on your needs and the constraints governing your international contracts. Please do not hesitate to contact us for advice on the best solution to use for your transactions. Our teams will be happy to provide you with the necessary guidance to ensure the successful completion of your transaction.

What are IBAN and BIC? How do they work?IBAN stands for International Bank Account Number. It is therefore an international standard for bank account numbering that enables the complete, consistent and unique identification of a bank account, regardless of the country or bank in which the account is held.

This system has only been in existence since 1997 and is now used in around 50 countries worldwide

BIC stands for Business Identifier Code. This is another standard that defines a universal code for identifying banking institutions. Every bank registered on the SWIFT system has a unique BIC code.

These two elements work together to ensure that financial transactions are carried out successfully, quickly, securely, reliably and in a traceable manner.

What are the naming conventions for IBAN and BIC? What elements do these two codes consist of?

The structure of an IBAN is standardised.

The length of an IBAN varies depending on the country where the bank account is held. It ranges from 14 to 34 characters. A Swiss IBAN, for example, is 21 characters long, compared with 27 for a French IBAN or 22 for a German IBAN.

The structure of an IBAN is standardised, although additional information may be included. As each IBAN specifies the country, the bank and the target account, it is therefore unique.

Depending on the country, the IBAN may include additional information. In France, for example, it is possible to identify the branch where a bank account is held.

The composition of a BIC is also standardised.

A BIC, on the other hand, is a standardised code, and this code does not vary in any way depending on the country of residence or the bank.

However, it is common for a bank to provide a BIC code without the branch code, as the latter merely indicates a geographical location and can generally be replaced by ‘XXX’ or even omitted altogether.

How do you check an IBAN?

At b-sharpe, we always check the IBAN you enter in your customer portal. There are also numerous websites where you can check or calculate the IBAN of a supplier or one of your customers.

We recommend using IBAN Calculator, for example. This website offers a comprehensive and reliable service for verifying IBANs.

Where can I find our IBANs?

Our IBANs for bank transfers are available directly in your customer portal under the ‘b-sharpe bank accounts’ section. We have put together a guide to help you find the IBANs in your customer portal.

Differences and similarities with the RIB

A bank account details statement (RIB) is a document provided by your bank that summarises all the information relating to your bank account. It usually includes not only your IBAN and BIC, but also your surname, first name, address, account number, and the name and address of the bank.

To carry out a transaction, only the IBAN, the BIC, the beneficiary’s name and their address are required. All other information is purely optional.