Swiss cross-border workers: the complete guide to working in Switzerland and living in France

- Swiss cross-border workers: what exactly are we talking about?

- Where to start? The essential steps

- Your salary is paid in CHF: how can you transfer it home without losing out?

- Taxes: France or Switzerland? The answer depends on your canton

- CMU or LAMal: a choice you can’t afford to get wrong

- Pensions: how does the Swiss system work for cross-border workers?

- Cross-border workers earn more, but at what cost?

- Frequently asked questions about life on the Swiss border

Working in Switzerland and living in France: the dream of a Swiss salary often comes up against a complex administrative reality.

• Considering working in Switzerland from France? Here's what no one tells you before you sign.

• G permit, taxes, health insurance, salary repatriation: four topics you absolutely must master.

• A few decisions made in the first weeks can cost you (or earn you) several thousand euros per year.

- Swiss cross-border workers: what exactly are we talking about?

- Where to start? The essential steps

- Your salary is paid in CHF: how can you transfer it home without losing out?

- Taxes: France or Switzerland? The answer depends on your canton

- CMU or LAMal: a choice you can’t afford to get wrong

- Pensions: how does the Swiss system work for cross-border workers?

- Cross-border workers earn more, but at what cost?

- Frequently asked questions about life on the Swiss border

Between the irreversible choice of health insurance, the tax complexities that vary from canton to canton, and exchange rate charges that erode your purchasing power, becoming a cross-border worker is not something you can just wing.

By the end of 2024, more than 407,000 of you had already taken up this daily challenge.

To turn this lifestyle into a genuine financial opportunity without getting overwhelmed, thorough preparation is essential. Driving licences, tax, salary repatriation and pensions: we’ve summarised everything you need to know to make a successful move.

Let’s get straight to the point.

Swiss cross-border workers: what exactly are we talking about?

One foot in France, a job in Switzerland

Becoming a cross-border worker means choosing a bicultural lifestyle: you work in Switzerland, but your main home remains in France.

Legally, this status is governed by specific rules.

Under bilateral agreements, to be considered a cross-border worker, you must return to your home in France at least once a week.

The key to working here is a G permit. This work permit, which is essential for EU/EFTA nationals, is linked to your employment contract and is obtained by your employer from the cantonal authorities.

Whether you’re planning to work in Geneva or another canton, this status allows you to take advantage of opportunities in the Swiss job market whilst maintaining your lifestyle in France.

It’s a balancing act that requires a certain amount of organisation, particularly when it comes to managing your day-to-day life across two currencies and two administrative systems.

400,000 cross-border workers: a phenomenon that is constantly growing

Cross-border work is far from being a minor phenomenon; it is a major trend that is gathering pace.

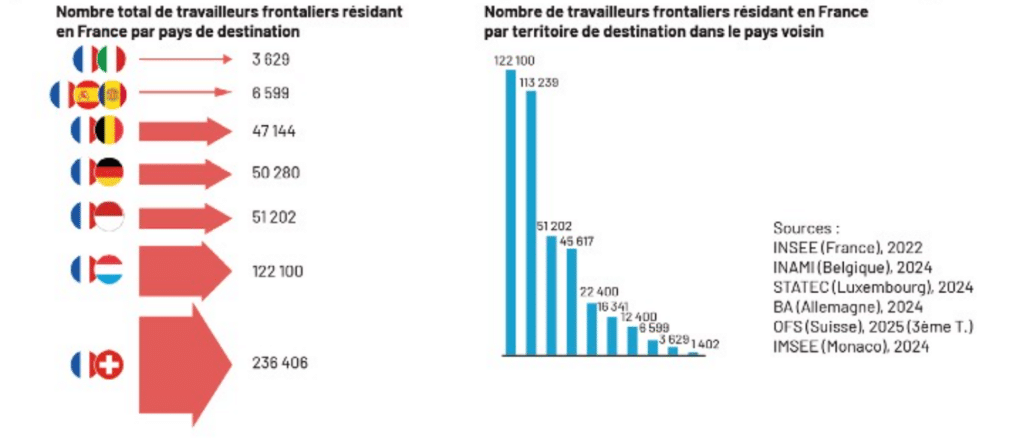

At the end of 2024, Switzerland had around 407,000 cross-border workers, a figure that is steadily rising.

According to its latest press release (April 2026), the Cross-Border Operational Mission (MOT) states that this figure has risen to 520,000.

Source: Press release 2026 – MOT

France is, in fact, the main country of residence for these workers: more than 236,000 of us (around 58% of all cross-border workers in Switzerland) cross the border every day.

Source: Cross-Border Operational Mission (MOT) – Manifesto for the balanced economic development of cross-border regions.

This growth is particularly pronounced in the canton of Geneva, which welcomed 8,000 new cross-border workers between 2023 and 2024.

Driven by dynamic sectors such as healthcare, finance, watchmaking and manufacturing, this lifestyle is attracting an increasing number of professionals seeking new challenges, to the extent that it is permanently transforming the regions of Haute-Savoie, Ain, Jura and Haut-Rhin into genuine economic powerhouses.

How much does a cross-border worker actually earn?

This is often the first thing that strikes people: Swiss salaries are among the highest in the world.

To be specific, the average salary in Switzerland is around CHF 5,488 per month (approximately €5,734).

In some cantons, such as Geneva, a minimum wage (although not officially recognised at federal level) is in place, amounting to CHF 4,368 gross per month.

An important point to note: if we take the national median wage (across all sectors) published by the FSO in 2024, it is higher: CHF 7,024 gross per month.

Source: The median wage in Switzerland in 2024.

However, to assess what you ‘really’ earn, you need to look beyond your gross salary. Working as a cross-border worker involves costs and choices that affect your actual budget:

Expenses to be deducted from the amount paid by your employer

Currency exchange fees

Your salary is paid in Swiss francs, but your expenses are in euros. Without a competitive currency exchange solution, bank charges can eat into a significant portion of your income.

Cost of journeys

Transport is a major expense. Between vehicle maintenance, fuel and any tolls, the cost can run to between €400 and €500 a month if you drive.

Health insurance

This is a requirement. You will need to choose between the French system (CMU) and the Swiss system (LAMal). This choice, which is often irrevocable, must be based on your personal circumstances and your income level.

In short, whilst the financial benefits are undeniable, they require careful management to become a genuine driver of quality of life.

Where to start? The essential steps

The G permit: your ticket to working in Switzerland

To work as a cross-border worker, you must obtain a G permit (cross-border worker permit).

Once your contract has been signed, your employer will submit the application to the relevant cantonal office.

What you need to know in practice:

- Validity: It is generally valid for five years if you have a permanent contract or a contract lasting more than one year. If your contract is shorter, the licence’s validity period will match the duration of your employment.

- Flexibility: If you change employer or move to a different canton, your permit can be updated fairly easily, provided you remain in the cross-border worker category.

- Requirement: You must return to your home in France at least once a week.

If you’re looking for a job in Geneva, find out what you need to know about working there.

Where should you live in France if you want to work in Switzerland?

Choosing where to live is a strategic decision, as it affects your commute and your budget. The most popular areas remain Haute-Savoie (Annecy, Annemasse, Saint-Julien-en-Genevois), Ain (Pays de Gex) and Haut-Rhin for the Basel area.

To make the right choice, bear these two factors in mind:

- Transport costs: Travelling from Annecy to Geneva by car can cost between €400 and €500 a month (petrol, wear and tear, tolls).

Do consider checking whether the Léman Express or cross-border bus services are nearby to help reduce these costs. - Housing costs: The closer you are to the border, the higher the rents.

For example, a four-and-a-half-room flat in Annemasse rents for an average of around €1,870, compared with €2,320 in Viry. To find out more about moving to the area, see our guide to becoming a cross-border worker.

Working from home: how far can you go without taking risks?

Working from home has become the norm for many, but it is strictly regulated for cross-border workers to prevent any changes in tax or social security arrangements.

The current rule of thumb is the 40% threshold of annual working time.

If you stay below this limit (i.e. around two days a week), you will continue to be taxed in accordance with the standard agreements between France and Switzerland and will remain registered with the social security system of the country where you work.

If you exceed this threshold, the implications can be complex: your employer may have to pay social security contributions in France, and your tax liability may change.

So please stay alert and discuss this with your employer to finalise your remote working agreement.

Unemployment among cross-border workers: your rights if you lose your job

It’s a question that often causes concern, yet the system is well-established.

If you lose your job in Switzerland, it is France (your country of residence) that will pay your benefits, not Switzerland.

Here are the steps to follow:

- Ask your former employer and the Swiss unemployment insurance fund for form PDU1 (or E301). This document summarises your periods of employment and your contributions in Switzerland.

- Register with France Travail (formerly Pôle Emploi).

- Your benefits will be calculated on the basis of your Swiss earnings, but in accordance with French rules.

Although Swiss employment law is more flexible (it is easier to dismiss staff there than in France), the job market is very dynamic: in 2024, the average time taken to find a new job in Switzerland was estimated at less than six months.

Your salary is paid in CHF: how can you transfer it home without losing out?

Why is your employer asking you for a Swiss personal IBAN?

This is one of the first administrative procedures you will have to deal with.

In Switzerland, the vast majority of employers require your salary to be paid into a local bank account with a Swiss IBAN starting with CH.

Why this requirement? For the sake of simplicity and cost-effectiveness.

Cross-border transfers to foreign accounts (even within the SEPA area) may incur administrative charges and result in longer processing times for the company.

Having a bank account in Switzerland also makes it easier to pay your local bills (such as your KVG health insurance) and manage your direct debits. It is therefore an essential prerequisite for getting your career as a cross-border worker off to a smooth start.

The monthly habit: converting your CHF at the right rate

Once your salary in Swiss francs is safely tucked away in your Swiss bank account, the all-important question arises: how do you transfer it to your French bank account in euros?

The usual approach is to use a standard bank-to-bank transfer.

This is often the most expensive option. Traditional banks generally charge:

- Fixed or proportional transfer fees.

- A spread on the exchange rate, which is the difference between the actual market rate and the rate they offer you.

When it comes to a monthly salary, even a few pence’s difference in the exchange rate can amount to tens, or even hundreds, of euros in lost income each month.

To make the most of your budget, it is essential to compare interest rates and not let your bank dictate the cost of borrowing.

What b-sharpe actually changes on your payslip

Using b-sharpe isn’t just about switching platforms; it’s about regaining control over the value of your work.

In practical terms, for a cross-border worker wishing to work in Geneva or elsewhere in Switzerland, our service offers three immediate benefits:

- More euros for the same effort: Thanks to our highly competitive and transparent exchange rates, you’ll receive a larger portion of your net salary once it’s converted into euros.

- No hidden fees: You know exactly what you’re paying. No nasty surprises when the money arrives in your French bank account.

- Simple and quick: The process is 100% online. You can make your transfer in just a few clicks, and your funds are converted and transferred quickly.

In short, b-sharpe acts as a natural extension of your payslip: we ensure that your Swiss salary is accurately reflected in your purchasing power in France.

Taxes: France or Switzerland? The answer depends on your canton

Taxation is often a source of many questions for newcomers.

In reality, where you pay your taxes does not depend on your nationality, but on the canton where you work and the tax agreements in force.

Cantons with withholding tax: Geneva leads the way

If you work in the canton of Geneva, tax is deducted directly from your salary each month.

This is known as pay-as-you-earn tax. The employer deducts the amount due and pays it to the cantonal tax authority.

⚠️ Please note: even if you pay tax in Switzerland, you are still required to declare your income in France.

To avoid double taxation, France grants you a tax credit equal to the amount of French tax. To understand all the intricacies of this status, see our guide to becoming a cross-border worker.

💡 Good to know:

The cantons of Aargau, Zurich and Schaffhausen also apply this withholding tax rule.

The 1983 Agreement: the cantons where you pay your taxes in France

To make life easier for cross-border workers, a specific agreement was signed in 1983. It covers eight cantons: Vaud, Valais, Neuchâtel, Jura, Bern, Basel-Stadt, Basel-Landschaft and Solothurn.

If you work in one of these cantons and commute home to France every day (or at least once a week), you pay all your income tax in France.

Switzerland therefore waives the withholding tax.

To qualify for this scheme, you must provide your Swiss employer with a certificate of tax residence (form 2041-AS).

Income tax returns: the forms you need to know about

Even if you already pay tax in Switzerland, you are still required to file a tax return in France in order to determine your overall tax rate (RFR). Here are the key documents:

- Forms 2042 and 2042-C: To declare your total income.

- Form 2047: Essential for declaring your income received abroad.

- Form 2041-AS: The certificate of residence required for cantons covered by the 1983 agreement.

Remember to keep your Swiss payslips and your annual salary statement, as these will serve as supporting documents for the French authorities.

Adjustment of tax at source

For cross-border workers subject to tax at source (particularly in Geneva), the standard tax scale does not always take your actual circumstances into account (actual expenses, third-pillar contributions, maintenance payments, etc.).

You have the option of requesting a correction to your withholding tax (or applying for a subsequent ordinary tax assessment – TOU).

This must be done by 31 March of the year following the year in which your income was received.

This could enable you to reclaim some of the tax you’ve paid if you have significant deductions. It’s a technical process, but one that can often be very beneficial for your annual budget.

CMU or LAMal: a choice you can’t afford to get wrong

This is undoubtedly the most important decision you’ll make in your new life as a cross-border worker.

Unlike other decisions, your choice of health insurance is, in the vast majority of cases, irrevocable.

Take the time to do your calculations.

Three months to decide: the right of option explained

From your first day of work in Switzerland (or from the date you take up residence in France), you have three months in which to exercise your “right of option”.

This right allows you to choose between:

- The French system: CMU (Universal Health Cover) for cross-border workers.

- The Swiss system: the LAMal (Health Insurance Act).

⚠️ Please note: if you do not make your choice within this timeframe, you will automatically be enrolled in the Swiss health insurance scheme (LAMal), often with no option to change your mind.

Universal Health Cover for cross-border workers: how it works and the costs involved

The CMU (administered by the CPAM in France) is based on solidarity.

The cost is not fixed: it is calculated based on your reference taxable income (RFR).

- Cost: The contribution currently amounts to 8% of your income (after a standard administrative deduction). The higher your Swiss salary, the higher your CMU contribution.

- The advantage: This is often the most cost-effective option for cross-border workers on modest incomes or those with several dependants (children, a non-working spouse), as the contribution covers the whole family at no extra cost.

Health Insurance for Cross-Border Workers: How It Works and the Costs Involved

Unlike in France, the Swiss LAMal operates on a per-capita premium basis, regardless of your income.

- Cost: You pay a fixed monthly premium (expect to pay around CHF 160 to CHF 200 for an adult, depending on the specialist cross-border health insurance provider).

- The advantage: Mathematically speaking, this is the most cost-effective option if you have a high income, as the premium does not increase in line with your earnings. However, each family member must pay their own premium (there are no free dependants).

What do these two schemes cover?

The choice isn’t just about price, but also about the flexibility of your care:

Under the CMU

- You will receive treatment in France in accordance with the National Health Service’s rates.

- You will only be able to receive medical treatment in Switzerland in an emergency; otherwise, you will be responsible for the costs.

Under the LAMal

- You have dual cover. You can receive medical treatment in France (using your Vitale card) AND in Switzerland (for example, to see a specialist or give birth in a Swiss clinic).

- This is a significant advantage for those who wish to benefit from the proximity of Swiss medical facilities.

Pensions: how does the Swiss system work for cross-border workers?

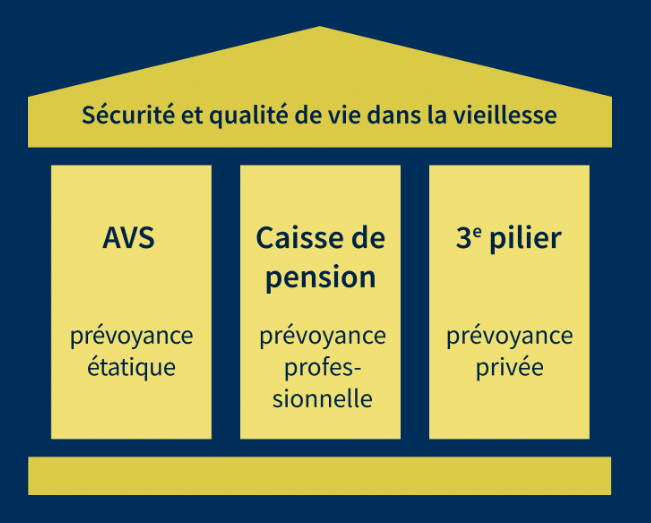

The Swiss pension system is based on the “three-pillar” principle.

Source: www.ch.ch

Unlike the French system, it skilfully combines national solidarity with individual capitalised savings.

Pillar 1 (AVS): the basic pension

Old Age and Survivors’ Insurance (AVS) is compulsory for all workers in Switzerland. It is designed to cover basic living expenses during retirement.

- How it works: It is based on a pay-as-you-go system. Your current contributions fund the pensions of today’s retirees.

- Key point for you: To receive a full pension, you must have made contributions continuously for 21 years up to retirement age. Each missing year will reduce the amount of your future pension proportionally.

The 2nd pillar (LPP): occupational pension provision

This is where the Swiss system stands out. The LPP is a funded savings scheme managed by a pension fund (foundation) set up by your employer.

- How it works: The money you pay in (and the amount your employer contributes) is placed into a personal account. This accumulated capital belongs to you.

- Practical benefit: Under certain conditions, you can withdraw all or part of this capital early, particularly to finance the purchase of your main residence. This is a powerful tool for becoming a cross-border worker and settling in with peace of mind.

The third pillar: voluntary savings

The third pillar is a private pension scheme designed to supplement the first two pillars, enabling you to maintain your current standard of living once you retire.

- Why take it out? The first and second pillars often only cover 60% of your final salary. The third pillar bridges this gap.

- Taxation: As a cross-border worker, opting for a "3rd pillar A" scheme may allow you to deduct your contributions from your taxable income (depending on your canton and tax status), thereby reducing your immediate tax bill.

Cross-border workers earn more, but at what cost?

The prospect of working as a cross-border commuter is appealing because of the salaries, but it requires a careful balance between financial gain and quality of life.

The financial and professional benefits

Working in Switzerland means gaining access to an extremely dynamic and rewarding job market.

- Salary: This is the number one selling point. For the same role, salaries in Switzerland can be two to three times higher than those in France.

- Career progression: Swiss corporate culture values competence and offers rapid career progression for motivated individuals.

- The working environment: The facilities and working conditions (tools, management) are often of a very high standard.

The challenges of everyday life

This is where you need to be realistic so as not to burn yourself out.

- Journey time: Crossing the border can be a daily challenge. Between queues at customs and congested roads, your journey time can be extended by two to three hours. Consider the Léman Express if you’re planning to work in Geneva.

- The "hidden" cost of living: If you live in neighbouring France, rents and prices in local shops are often linked to Swiss wages. Your purchasing power may be eroded by this local inflation.

- Flexibility in employment law: In Switzerland, dismissal is much simpler and quicker than in France. Job security depends primarily on your performance.

- The 42-hour working week: The statutory working week is longer than in France (often 42 hours compared to 35). This is something you’ll need to factor into your family life.

Key takeaways:

Cross-border worker status offers exceptional financial benefits, provided you understand the rules. From managing your G permit to making strategic choices about your health insurance, every decision has a direct impact on your disposable income.

Don’t let bank charges and arbitrary exchange rates undermine all your hard work. Plan ahead, optimise your salary remittances and secure your future.

Ready to take the plunge? Start by opening your Swiss bank account and compare the options for converting your first Swiss francs at the best rate right now.

Frequently asked questions about life on the Swiss border

The national median salary in Switzerland is CHF 7,024 gross per month (FSO data for 2024).

This figure varies by canton and sector: in Geneva, for example, the minimum wage is set at CHF 4,427 gross (indexed amount for 2024) for a 40-hour working week.

We have analysed the FSO’s official press release on the Swiss median wage (gross monthly by sector of activity) to provide you with a useful summary, whatever your circumstances:

• National average (all sectors): CHF 7

,024• Senior management roles: CHF 10,

750• Non-management roles: CHF 6

,014• Simple tasks (no training required): CHF 5

,618• High value-added sectors: CHF 10,

000• Service sectors (Hospitality): < CHF

5,500 Data source: https://www.admin.ch/fr/newnsb/CzozNgBTCJOrNyvwsItyp

It all depends on the canton where you work.

In Geneva, as well as in the cantons of Aargau and Zurich, tax is deducted at source from your salary.

In the cantons covered by the 1983 agreement (such as Vaud, Valais and Neuchâtel), you pay your taxes in France.

In both cases, you are required to declare your income in France.

Your employer pays your salary in CHF into a Swiss bank account (IBAN starting with CH). To transfer this money to your French account in euros without incurring the high exchange fees charged by traditional banks, the most effective solution is to use a specialist online currency exchange platform such as b-sharpe.

You can work remotely for up to 40% of your annual working time (i.e. approximately 2 days per week) without this affecting your tax status or your social security contributions. Exceeding this threshold may result in a change of tax status in France and additional social security contributions for your employer.

Yes.

If you lose your job, you will receive benefits from your country of residence, France, in accordance with the rules of France Travail (formerly Pôle Emploi).

To claim your benefits, you must request the PDU1 form from the relevant Swiss unemployment insurance fund at the end of your contract.

Your contributions to the 1st pillar (AVS) are retained in Switzerland and will be paid to you as a pension when you reach retirement age.

For your 2nd pillar (LPP), you can either leave the capital in a vested benefits account in Switzerland or request a lump-sum payment under certain conditions (setting up a business, purchasing a main residence or leaving the European Economic Area permanently).

On the same topic