Interbank exchange rates: optimising your foreign exchange transactions

- What is the interbank exchange rate?

- How is the interbank rate set?

- Supply and demand: what causes exchange rates to fluctuate

- Why aren’t you eligible for the interbank rate?

- The exchange rate margin: how is it calculated?

- How can you find out how much you’ll receive?

- When should you carry out currency exchange transactions?

- 3 costly mistakes to avoid when trading currencies

- Spot rates and forward rates: what’s the difference?

- How can I get the best exchange rate?

When converting currencies, you soon realise that the amount you receive is significantly lower than the figure shown on Google. The culprit? The exchange margin.

• The reference rate: the interbank exchange rate represents the "raw" market price used in transactions between major financial institutions.

• The exchange margin: as a user, you pay a "spread" that corresponds to the intermediary's remuneration to cover its costs and the risks of volatility.

• Cost comparison: while traditional banks apply margins often between 2% and 5%, digital solutions like b-sharpe make it possible to reduce these fees to as low as 0.5%.

• Transparency watch: so-called "fee-free" offers conceal a significant markup on the real exchange rate.

• Risk management: to protect your purchasing power, you can use the spot rate for an immediate need or the forward rate to lock in a rate for a future transaction.

- What is the interbank exchange rate?

- How is the interbank rate set?

- Supply and demand: what causes exchange rates to fluctuate

- Why aren’t you eligible for the interbank rate?

- The exchange rate margin: how is it calculated?

- How can you find out how much you’ll receive?

- When should you carry out currency exchange transactions?

- 3 costly mistakes to avoid when trading currencies

- Spot rates and forward rates: what’s the difference?

- How can I get the best exchange rate?

The difference in fees between banks and bureaux de change can turn a simple transaction into a net loss of several hundred euros.

The way to protect your budget is to understand and aim for the interbank exchange rate, which is the true market price.

In this article, we explain how this rate is set, how to spot hidden fees, and how to optimise your conversions so you don’t leave money on the table.

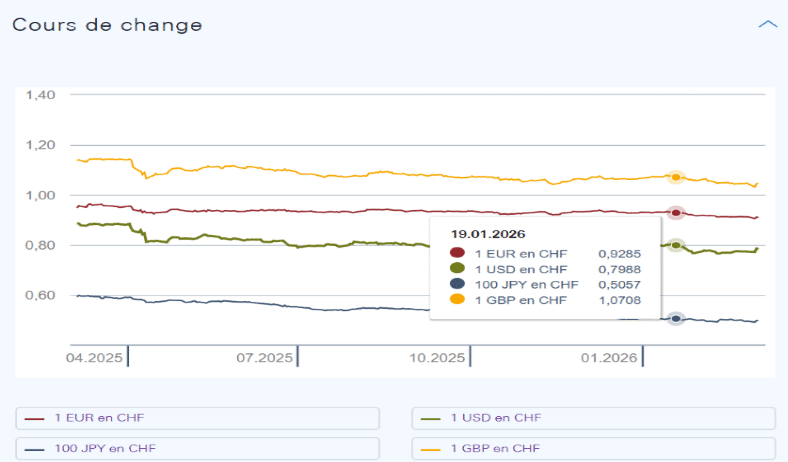

What is the interbank exchange rate?

The interbank exchange rate, often referred to as the ‘mid-market rate’, is the rate at which banks trade currencies with one another.

This ‘over-the-counter’ market operates 24 hours a day and forms the heart of the global financial system. It represents the gross reference value of a currency, with no mark-up added.

Source: Swiss National Bank (SNB)

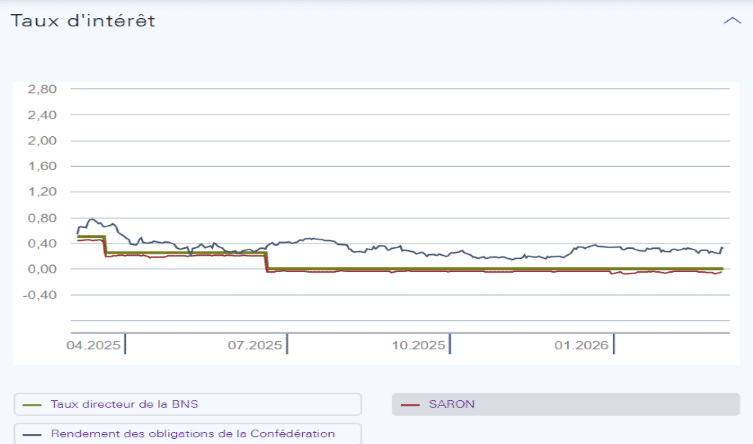

How is the interbank rate set?

Unlike the price of a product in a shop, the interbank rate is not set by a single central authority.

It is determined in real time on the interbank market by commercial banks, central banks and investment funds trading massive volumes of capital. The process is based on several key elements:

- Actual transactions: the rate is derived from the buying and selling prices used in interbank trading.

- The role of central banks: institutions such as the SNB influence exchange rates through their monetary policy, in particular by adjusting key interest rates to steer the cost of borrowing in the market.

- Liquidity: banks with surplus funds lend them to those in need, creating a constant flow that stabilises or causes fluctuations in the currency’s value.

Source: Swiss National Bank (SNB)

Supply and demand: what causes exchange rates to fluctuate

The fluctuation in rates follows a simple economic principle of supply and demand:

- Demand is rising: if many market participants wish to buy a particular currency (to invest in the country, purchase assets, or because a rise in key interest rates has made the currency attractive), its value rises.

- Supply increases: conversely, if holders of a currency seek to offload it en masse, its price falls.

Why aren’t you eligible for the interbank rate?

It is impossible for an individual or a business to obtain the interbank rate directly for their day-to-day transactions. Here’s why:

- A question of volume: the interbank rate is reserved for transactions involving millions, or even billions, of currency units. The volumes traded by private individuals are too small to gain access to this wholesale market.

- The intermediary’s margin: to process your request, retail banks and bureaux de change apply a profit margin and cover their operating costs.

- Currency risk: the intermediary bears the risk associated with exchange rate volatility, which fluctuates every second.

In short, the interbank rate is the benchmark, whilst the “customer” rate always includes service and transaction fees.

The exchange rate margin: how is it calculated?

Understanding the exchange margin is essential for assessing the true cost of a currency conversion.

It represents the difference between the interbank rate (the wholesale price) and the rate quoted for your transaction.

The margin mechanism

The exchange rate spread constitutes the financial intermediary’s fee. It is calculated as the difference between the buying price and the selling price of a currency.

In practical terms, the financial institution buys foreign currency at the interbank rate and sells it to you at a slightly higher price (or buys it back from you at a lower price).

This difference covers operating costs, risks associated with market volatility and the profit margin.

This spread is generally wider for low-volume trades or ‘exotic’ currencies.

Comparison of margins: banks vs. bureaux de change vs. online services

Comparison of foreign exchange brokers

Traditional banks

Interest rate spread

Significant (usually between 2% and 5%).

Additional charges

Fixed fees charged per transaction.

Justification of costs

Traditional banking cost structure.

Currency exchange bureaux

Interest rate spread

Very high (especially at stations and airports).

Additional charges

Included in the margin or administration fee.

Justification of costs

High fixed costs: rent and the physical storage of banknotes.

Online services (such as b-sharpe)

Interest rate spread

Reduced (sometimes close to the interbank rate).

Additional charges

Complete transparency, often with no hidden costs.

Justification of costs

Digital infrastructure optimised to reduce costs.

Hidden costs to watch out for

It is important to be vigilant, as the total cost is not always limited to the percentage shown.

There may be a number of hidden charges:

- The inflated exchange rate: this is the most common hidden charge. A provider may advertise ‘0% commission’ whilst applying an exchange rate that is far removed from the interbank rate.

- Transfer fees: in addition to the margin on the exchange rate, sending or receiving fees may be charged for international transfers.

- Correspondent bank charges: when making a transfer outside the SEPA zone, intermediary banks may charge fees without giving you prior notice.

- Fixed fees: some providers charge a fixed amount per transaction, which is particularly disadvantageous for small amounts.

By identifying these hidden bank charges, you can effectively compare offers to protect your budget.

How can you find out how much you’ll receive?

To estimate the exact amount of a conversion, it is important to bear in mind that the final rate depends on the intermediary chosen.

This exchange rate answers a simple question: “How many Swiss francs (CHF) do I need to pay to get 1 €?”

The formula for calculating the exchange rate

The calculation of a real exchange rate includes the intermediary’s margin on the current interbank rate.

- Rate applied = Interbank rate × (1 + intermediary’s margin %)

Once you have this rate, the calculation to work out your final amount is as follows:

- Amount received (€) = Amount sent (CHF) / Exchange rate applied

💡 Good to know:

If you carry out the reverse transaction (from euros to Swiss francs), the process is reversed: you divide the interbank rate by the margin, then multiply the amount sent by this new rate.

A practical example involving different intermediaries

For a conversion of CHF 10,000 at an interbank rate of 1.12, for example, the results vary depending on the margins:

A cost breakdown for the same transfer

Traditional bank

- Margin applied: 2%

- Final exchange rate: 1.1424

- Net amount received: €8,753.50

Currency exchange

- Margin applied: 0.9%

- Final exchange rate: 1.1301

- Net amount received: €8,848.77

Option b-sharpe

- Margin applied: 0.5%

- Final exchange rate: 1.1256

- Net amount received: €8,884.15

The difference is striking: for the same amount at the same time, the gap between a bank and an optimised solution amounts to €130.65.

The impact of the margin on a monthly budget

These exchange rate differences, which may seem minor at first glance (just a few pence on a rate), have a significant impact over time.

Whether you’re transferring wages from Switzerland or making regular payments, choosing the most competitive solution is a direct way to save money.

According to our figures, using an optimised digital solution such as b-sharpe rather than your bank allows you to save over €130 on a single transaction of CHF 10,000. As a result, any user – and particularly those who have recently become cross-border workers in Switzerland – can achieve a considerable gain in purchasing power over a full year by eliminating these excessive margins.

When should you carry out currency exchange transactions?

The foreign exchange market is constantly in flux.

Whether you are an individual or a business, choosing the right time to convert your funds requires an understanding of the factors that drive prices up or down.

Factors influencing exchange rates

The exchange rate reflects a country’s economic health and stability.

Several key factors account for these variations:

- Interest rates: when a central bank raises interest rates, it makes its currency more attractive to investors, which boosts demand and drives up the exchange rate.

- Inflation: as a general rule, a country with a low and stable inflation rate sees its currency appreciate against those of its trading partners, as its purchasing power is better maintained.

- Political and economic stability: investors seek security. In times of crisis, the Swiss franc (CHF) acts as a ‘safe haven’, causing its value to rise automatically.

- The trade balance: if a country exports more than it imports, demand for its currency increases, which strengthens its exchange rate.

- Public debt: massive levels of debt can scare off investors, leading to a sell-off of the currency and a fall in its value.

Should we try to time the market?

“Market timing” involves attempting to predict the highest or lowest point in order to take action.

In practice, this is an extremely risky strategy, even for professionals, as financial markets react instantly – and sometimes irrationally – to global news.

Trying to predict the exact movement of exchange rates takes a considerable amount of time and leaves one open to costly mistakes.

A common misconception is that one can consistently beat the market; however, given the high level of volatility, it is often wiser to adopt a disciplined approach rather than a speculative one.

For most users, the aim is to get a fair and transparent rate rather than chasing a ‘perfect price’ that only exists for a brief moment.

Interest rate alerts: a strategy for smoothing out operations

Rather than simply weathering market volatility, a prudent strategy involves anticipating your needs to capitalise on the best opportunities, whilst spreading your transactions over time to average out your exchange rate over the year.

To avoid being glued to the charts, automatic monitoring via rate alerts allows you to regain control without any stress.

With this in mind, b-sharpe offers customisable alerts via its customer portal and mobile app to track currency movements.

You will receive a notification as soon as the exchange rate reaches the level you consider acceptable, helping you to maximise your conversions.

3 costly mistakes to avoid when trading currencies

Optimising your foreign exchange transactions is about more than just finding a good rate.

Many users lose a significant portion of their capital by falling into common traps associated with the way financial intermediaries operate.

Relying solely on the advertised rate

The most common mistake is to focus solely on the figure displayed on the scoreboard or the home screen.

A rate may seem attractive whilst masking a different reality:

Some providers use introductory rates that differ from those actually applied during the final transaction, particularly during periods of market volatility. To avoid these common errors in foreign exchange transactions, it is crucial to check the net amount you will actually receive in your account rather than confirming the transaction based solely on a marketing display.

Ignore additional charges

The exchange rate is just one component of the total cost. Ignoring ancillary costs is a mistake that takes a heavy toll on the budget, particularly for cross-border workers:

- Transfer and receiving fees: fixed fees for sending or receiving foreign funds, regardless of the exchange rate.

- Fixed fees: administrative or transaction charges added by some bureaux de change.

- Account maintenance fees: annual management costs associated with certain specific accounts.

When added together, these so-called “hidden” costs can turn what appears to be a good deal into an expensive transaction.

Falling into the trap of loss-leader offers

The phrase ‘No commission’ or ‘No fees’ is one of the most dangerous pitfalls.

In reality, no service works for free: the fee is almost always hidden within a substantial mark-up on the exchange rate. This lack of transparency makes it difficult to compare offers effectively.

Rather than being tempted by advertised ‘free’ services, choose your currency exchange provider based on transparency: a provider that clearly states its margin on the interbank rate is often much better value than one where the actual margin is hidden.

Spot rates and forward rates: what’s the difference?

In the world of foreign exchange, the moment of decision is just as crucial as the moment of execution.

To address these timing issues, the financial market relies on the differences between spot and forward rates, two distinct mechanisms that enable the management of either immediate needs or future expectations.

The spot rate

The spot rate is the price of a currency for immediate delivery (usually within two working days).

This is the rate displayed in real time on trading platforms or online converters, reflecting supply and demand at any given moment.

This applies if you need to convert funds immediately for an urgent matter.

The forward rate

The forward rate allows you to fix an exchange rate today for a future transaction (in one month, six months or a year).

Contrary to popular belief, this is not a prediction of the future but a mathematical calculation based on the current spot rate and the interest rate differential between the two currencies.

This mechanism, often used in forward sales, locks in a price in advance and protects against unexpected price falls.

Which one should you choose, depending on your circumstances?

The choice between these two instruments depends on your financial situation and your risk tolerance:

- Choose the spot rate if: your funds are available immediately and you are happy with the current exchange rate. This is the ideal solution for day-to-day transactions with no time constraints.

- Choose the forward rate if: you are planning a large payment or receipt (property purchase, supplier payment, future salary).

The main advantage is that you can lock in an exchange rate to safeguard your budget. This removes the uncertainty associated with the volatility of the interbank market and allows you to know exactly how much you will receive in the future.

How can I get the best exchange rate?

Finding the best rate isn’t about looking for a figure that looks good on paper, but about identifying the offer that leaves you with the highest net amount after all fees have been deducted. Here are the steps to follow:

Compare brokers based on actual spreads

When assessing an offer, always compare it with the interbank rate. The difference represents the margin charged.

As many establishments do not state this figure explicitly, work it out for yourself:

Multiply your amount by the market rate, then compare the result with what the broker actually plans to pay into your account. It is by minimising this difference as much as possible that you will be able to secure the best exchange rate for your transaction.

Prioritise transparency regarding fees

An attractive rate can sometimes mask underlying costs. To maximise your conversion rate, insist on complete transparency on two points:

- The margin on the rate: this must be clearly stated.

- Transfer fees: some banks charge a fixed fee, which is particularly costly for small and medium-sized transactions.

Transparency is the best way to build trust.

A reputable service provider should be transparent about what they charge and what you will receive, with no hidden fees to eat into your capital.

The b-sharpe approach: spreads from 0.5% and no hidden fees

As a specialist provider, b-sharpe offers a direct alternative to traditional banking channels thanks to its optimised cost structure:

- A sliding-scale margin: The pricing system is simple and transparent. The margin on the interbank rate starts at 0.5% and can decrease depending on volume, whereas banks often charge 2% or more.

- No hidden fees: b-sharpe does not charge any administration or transfer fees on your transactions.

- Simple and fast: a secure foreign exchange account allows you to convert and transfer your funds quickly, enabling you to take advantage of interbank market opportunities in real time.

With b-sharpe, you keep more of your money, whether you’re a cross-border worker converting your salary or a business managing international payments.

On the same topic

Announcement from the Fed