Withdrawal from the 2nd pillar: exchange your CHF at the best rate

b-sharpe assists you with the withdrawal of your 2nd pillar (LPP) savings when you leave Switzerland. Your funds are converted at market rates and securely transferred to your account from Geneva by a dedicated team.

Competitive rates

No hidden charges

100% Swiss secure service

Protect the value of your pension

Withdrawing funds from a 2nd pillar pension often involves transferring several hundred thousand francs abroad. In this context, a bank margin of 1–2% on the exchange rate can cost you thousands of francs.

With b-sharpe, your pension assets are converted at the market rate, with a commission known in advance and dedicated support from Geneva.

Your retirement capital is used for your plans. Not for bank margins.

Changes to the 2nd pillar:

b-sharpe supports you every step of the way

When your 2nd pillar funds are paid out: receipt and conversion of your assets

When your pension fund or foundation releases your BVG capital, the funds are paid into your personal b-sharpe IBAN account.

With b-sharpe, you can:

• receive your assets securely in Geneva,

• convert them into the currency of your choice at market rates,

• track every step via your personal account.

Every transaction is carried out in accordance with Swiss security and compliance standards.

When transferring money abroad: secure transfer of your funds

Once converted, your assets can be transferred to the account of your choice (bank, solicitor, insurance company, etc.).

With b-sharpe, you can:

• send your funds in the currency of your choice, without opening a local account,

• benefit from a fast and secure transfer from Geneva,

• receive support from a team of Swiss experts every step of the way.

Our aim: to ensure that every franc of your pension goes towards your plans.

When and how can you access your 2nd pillar pension?

Are you planning to retire abroad?

- Depending on your pension fund, you may be able to request a partial or full payout of your 2nd pillar pension.

- The procedures and timeframes vary depending on the foundation.

You are moving to an EU/EFTA country

- Only the non-statutory portion can be withdrawn immediately if you are insured under a statutory scheme.

- The rest must remain in a tax-deferred account.

You are leaving Switzerland for a country outside the EU/EFTA

- In principle, you can withdraw your entire 2nd pillar pension.

- A certificate of permanent departure is usually required.

You are buying a main residence abroad

- Your 2nd pillar can finance the purchase under the EPL scheme, subject to your pension fund’s rules.

- Certain supporting documents will be required.

Swiss precision. The agility of a fintech company.

Your conversions and transfers go through a secure Swiss system with no hidden surprises. You remain in control at every stage, from the first click to the receipt of the funds.

A Swiss IBAN in your name

No more copying payment references. Transfer your funds just as easily as you would with a traditional bank account.

A 100% Swiss service

A secure solution and a Geneva-based team, serving you since 2013.

Save money on every transaction

Our rates are among the most competitive on the market. Everything is disclosed in advance, so you know exactly how much you will receive.

Over 40,000 satisfied clients

With an average rating of 4.8/5 on Trustpilot

They have tried b-sharpe

and recommend it

“Thank you for your clear explanations and your help in finalising my 2nd pillar transfer at the best rate.”

25 December 2022

Like thousands of individuals and businesses, exchange your currency at the best rate with b-sharpe.

✓ Verified review

I am very satisfied

I’m really glad I used b-sharpe to transfer my pension. Thank you very much.

11 July 2021

4.8/5 on Trustpilot

Over 3,000 verified reviews, not just empty promises

Withdrawing and switching your 2nd pillar

pension has never been easier.

- Create an account

- Sending funds

- Delivery within 24

hours, excluding weekends and public holidays

- NO account opening fees

- NO account management fees

- NO account closure fees

Everything you need to know

about withdrawing funds from the 2nd pillar

Find out how to convert and transfer your funds abroad with ease. Clear and concise articles to help you optimise your international transactions.

A closer look at the Swiss LPP for cross-border workers

Pillar 3: should you withdraw or continue contributing to it after leaving Switzerland?

Understanding how pensions work in Switzerland

Frequently

asked questions about withdrawing funds from the 2nd pillar

The mandatory portion corresponds to the minimum pension provision required by the LPP Act, with parameters set by law (coordinated salary, age-related bonuses, minimum conversion rate on retirement). The non-mandatory portion covers elements above the legal minimum (higher salaries or improved benefits) and is governed by the pension fund’s own regulations. It generally offers greater flexibility, but the conversion rates and conditions may be less favourable than for the mandatory portion.

The 2nd pillar can be withdrawn at retirement age (or early, depending on the fund), in the event of permanent departure from Switzerland, to finance a main residence, or when switching to self-employment. If moving to a country outside the EU/EFTA, the capital can in principle be withdrawn in full; when moving to the EU/EFTA, only the non-mandatory portion is generally paid out as a lump sum, with the mandatory portion remaining in a vested benefits account. There are special cases (disability, small amounts, divorce).

No, it is not possible to withdraw your 2nd pillar freely whilst remaining an employee in Switzerland. However, early withdrawal is permitted in certain specific cases: purchase of a main residence for personal use, transition to self-employment, or if the amount is very small. Apart from these situations provided for by law, the capital remains locked in until retirement.

You can withdraw your 2nd pillar savings if you leave Switzerland permanently. Your pension fund or foundation will then pay the capital into your personal b-sharpe IBAN, from where it is converted and transferred securely to your account abroad.

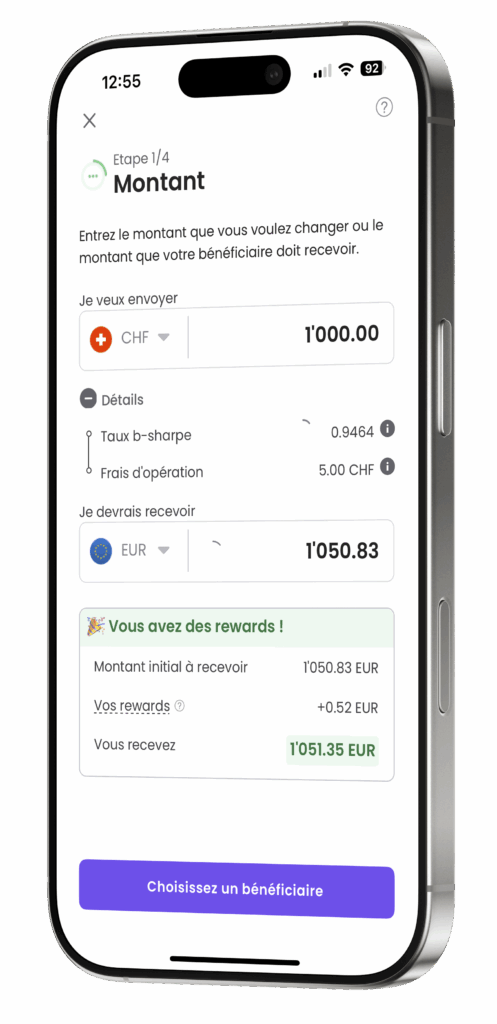

b-sharpe applies clear, sliding-scale transaction fees starting at 0.12%. Your funds are then converted at the current market rate, with no hidden or additional fees. The total cost is significantly lower than that charged by traditional banks.

A lump-sum withdrawal from the 2nd pillar is taxed separately from other income, at a reduced and progressive rate. If you are resident in Switzerland, tax is collected by your canton of residence. If you move abroad, a withholding tax is levied by the canton where the pension fund is based, with the possibility of a partial refund depending on the applicable tax treaties.

No. Thanks to your personal b-sharpe IBAN, your pension fund can pay your assets directly in Swiss francs before they are converted. You then transfer your funds in the currency of your choice (EUR, GBP, USD, etc.) to the destination account, without opening a local account.

There is no standard legal timeframe. Once the complete application has been approved by the pension fund, the payment is usually made within a few weeks (often 2 to 6 weeks). In the event of moving abroad, a withdrawal for housing purposes or a tax audit, processing may take longer depending on the complexity of the case.

b-sharpe is a Swiss financial intermediary, affiliated with SO-FIT, a self-regulatory organisation recognised by the Swiss Financial Market Supervisory Authority (FINMA). Your funds are held in a bank account domiciled in Switzerland, separate from b-sharpe’s own funds, and covered by insurance of CHF 5 million against fraud and hacking.