Its history is a fascinating tale, spanning from the monetary upheaval of the Napoleonic era to the establishment of a world-renowned currency.

Today, a robust economy, low levels of debt and the strategic management of the Swiss National Bank (SNB) ensure its stability.

Source: ProRealTime Web

The concept of a strong currency is entirely relative: a currency may be strong against one currency and weak against another.

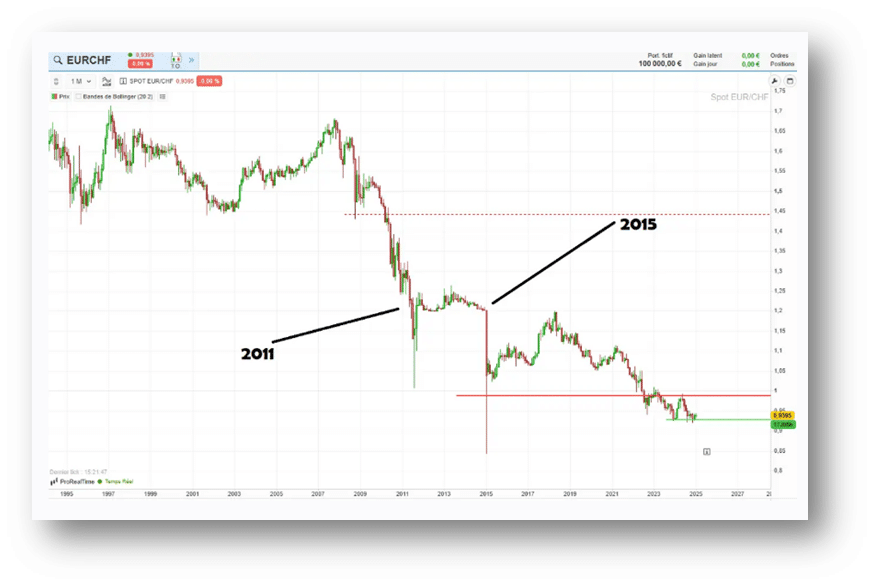

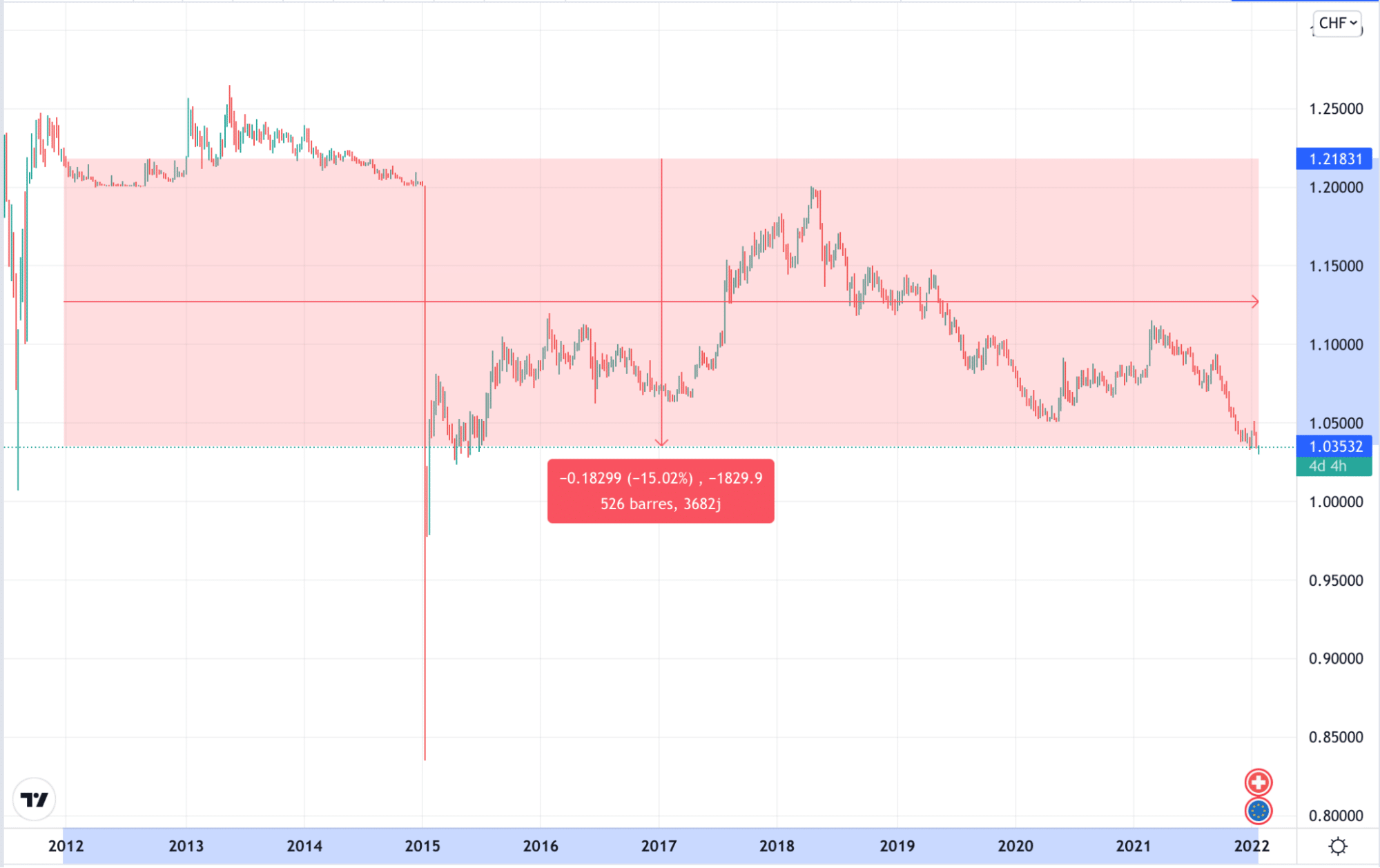

Take, for example, the EUR/CHF exchange rate (in other words, the value of one euro when converted into Swiss francs). At the start of 2012, it cost around 1,219 Swiss francs to buy 1,000 euros, but today it costs just 1,035 Swiss francs to buy the same amount.

Whilst both currencies can be considered strong in absolute terms, the Swiss franc has come out on top against the euro over the last decade, with a positive trend in the exchange rate against the single currency.

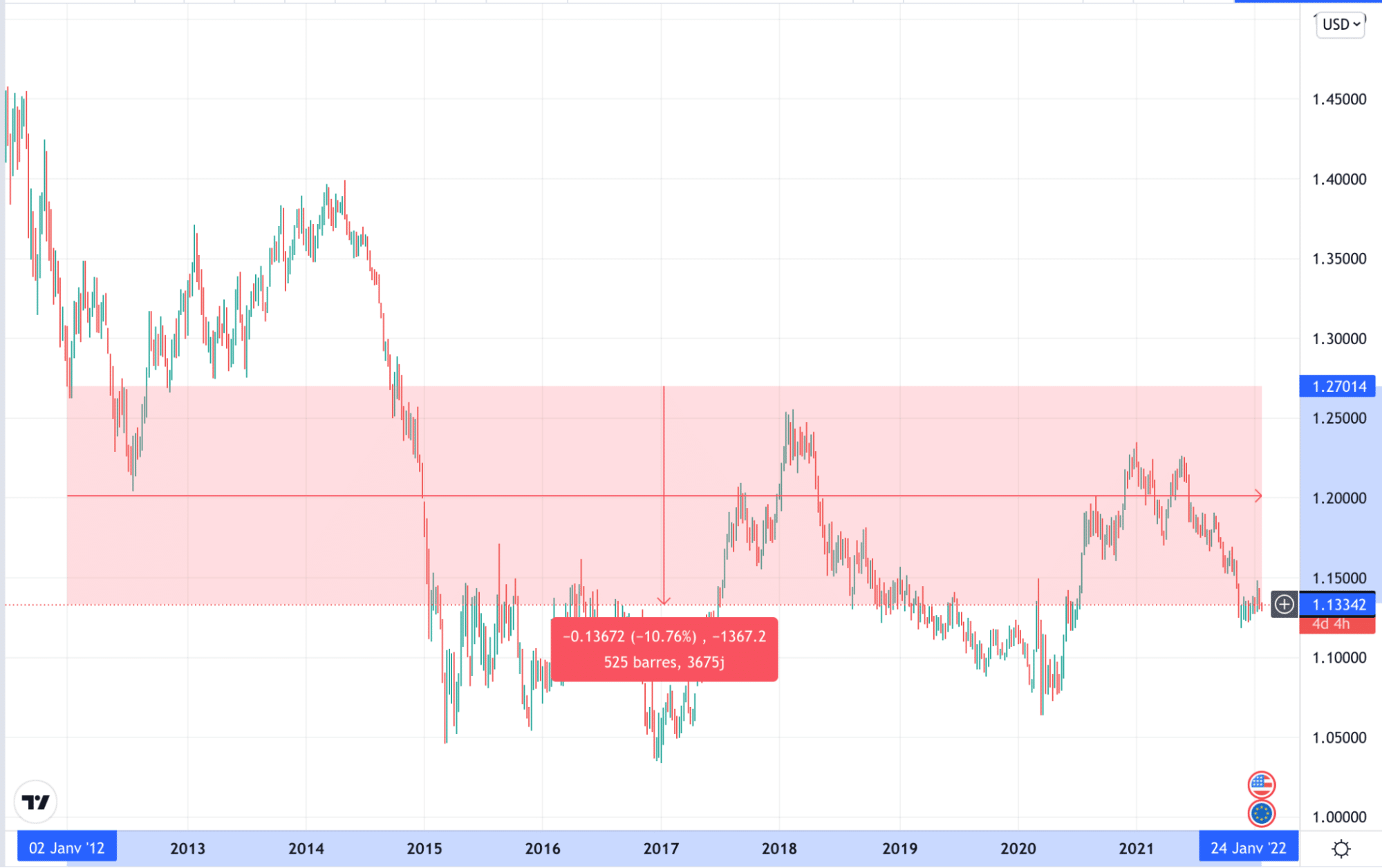

Another example: over the same period, it cost around $1,270 to get €1,000 in 2012, whereas today it costs just under $1,134 to get the same amount.

A History of the Swiss Franc in the 20th Century

From the 1920s to the Second World War

In the 1920s, European currencies collapsed one after the other, culminating in the German mark, which fell victim to the hyperinflation of the Weimar Republic, where, in 1923, the retail price rose by a factor of 750 billion over a period of 10 years. In other words, a baguette that had sold for 1 mark 10 years earlier now cost… 750 billion marks: a clear illustration of the currency’s loss of value!

Conversely, the Swiss franc, for its part, fully demonstrated its value as a safe-haven currency thanks to the maintenance of its gold standard, which increasingly attracted foreign investment.

By the late 1920s, the strength of the Swiss franc was not all good news: the export-oriented Swiss economy was hit hard by the high value of the Swiss franc, resulting in unemployment affecting more than 20% of the working population by the mid-1930s.

During the Second World War, Switzerland built up its gold reserves by selling raw materials to Germany in exchange for the precious yellow metal.

It was therefore during these 25 years that the Swiss franc laid the foundations for its strength.

Switzerland and the Bretton Woods Agreements

At the end of the war, Switzerland refused to sign up to the Bretton Woods Agreement (which pegged currencies to the dollar, with a link to gold), but the Swiss franc nevertheless remained one of the strongest currencies.

When, in 1971, the Bretton Woods agreements collapsed and currencies were subject to floating exchange rates (meaning that exchange rates were determined by supply and demand), the Swiss economy was in good health. Capital was pouring into Swiss banks from abroad, but Swiss companies, particularly those in the industrial sector, were once again facing very difficult times and unemployment in Switzerland was rising.

The oil crisis of the 1970s and the currency crisis of the 1990s

The oil crises of the 1970s sounded the death knell for the various measures devised by the Swiss National Bank (SNB) to curb the rise in the value of the Swiss franc. Switzerland’s economic difficulties persisted, compounded by the poor management of liquidity injections into the economy intended to mitigate the effects of the 1987 stock market crash.

The result was that the construction and property sectors began to overheat. To counter this, the SNB raised interest rates, plunging the country’s economy into a severe recession. Ultimately, the 1990s proved to be a very difficult period economically due to the interest rate cuts coming too late. Nevertheless, the Swiss franc held its ground against almost all other currencies.

The floor rate in response to the 2008 crisis

To address the fallout from the 2008 crisis, the SNB decided in 2010 to cut its interest rates to zero in order to safeguard the Swiss banking system and flooded the market with liquidity.

Despite this, the Swiss franc retained its status as a safe-haven currency and its value rose significantly against the euro and the dollar, forcing the SNB to introduce a floor against the euro (to protect Swiss exports) until the EUR/CHF floor suddenly collapsed in 2015.

The reasons why the Swiss franc is a strong currency

In the case of Switzerland, two key factors explain the strength of the Swiss franc relative to other currencies:

- economic growth; which has held up relatively well compared with the rest of the world and has managed to weather the recent crises without too much damage.

- low levels of debt; despite the crisis, Switzerland’s debt levels remain well below those of its European counterparts. Whilst Switzerland’s debt-to-GDP ratio does not exceed 30%, those of its neighbours are soaring, at 116.3% for France and 153.5% for Italy.

- the stability of the geopolitical environment. Unlike certain currency areas that are relatively unstable due to geopolitical factors and/or rampant inflation, Switzerland offers reassurance thanks to its high level of economic and political stability.

Switzerland, the Swiss franc and foreign capital

Countries with what is known as a strong currency all share one characteristic: they attract capital from foreign investors. The more foreign capital flows in, the stronger the currency becomes.

In 2020, foreign investment in Switzerland totalled more than 1,216 billion Swiss francs. In contrast, Switzerland invested more than 1,460 billion Swiss francs globally.

Switzerland is one of the world’s leading investors abroad. However, in 2019 and 2020, against the backdrop of the health crisis, Swiss companies repatriated 54 billion and 34 billion Swiss francs respectively, which helped to shore up the Swiss franc on the foreign exchange market.

Is the Swiss franc a safe-haven currency?

According to a study published by the CEPII, the Swiss franc is not as strong a currency as is commonly believed. To support this claim, they analysed the behaviour of the major currencies in crisis situations. These experts assumed that a safe-haven currency should generate a positive return during periods of crisis and a negative risk premium over the long term.

Based on this premise, analysts examined the performance of 26 currencies over a 15-year period, from 1999 to 2013. To everyone’s surprise, only two currencies, according to the analysis, behaved as safe-haven assets: the yen and the dollar.

Conversely, the Swiss franc, which tends to track movements in the euro, does not possess the characteristics of a safe-haven currency. Analysts point out, however, that this analysis predates the end of the EUR/CHF exchange rate floor. It can therefore be assumed that, once freed from its peg to the euro, the Swiss franc will perform better (and thus more positively) in times of crisis.

Alternatives to a Swiss bank account: how to manage your CHF without a traditional accountIn many cases, the answer is no. There are now simple and cost-effective ways to manage your Swiss franc (CHF) income, convert it quickly into euros (EUR) and transfer it to your French bank account.

Whether you’re making a purchase, investing, or receiving a regular salary, you can avoid the lengthy procedures and hidden fees associated with traditional banks.

With b-sharpe, the currency exchange specialist for cross-border commuters and Swiss residents, you take back control: lower fees, a transparent service and the ability to manage your life across two currencies… without losing out on hundreds of francs a year. Discover the best options available to you based on your profile.

Why choose an alternative to opening a bank account in Switzerland?

Before a French worker can receive their salary in Swiss francs, transfer it to their current account and convert it into euros, they must first take certain steps. To do this, they should ideally have:

- A Swiss bank account, in Swiss francs (CHF), for receiving your salary and, if necessary, making purchases in Switzerland.

- A French bank account, so you can have your salary paid into it in euros.

- A currency exchange service, so you can convert your Swiss francs into euros.

- A service enabling low-cost international money transfers between Switzerland and France

💡 How can I transfer my Swiss salary to France at the lowest cost?

There are several ways to do this:

• The most common method is to open a CHF account with a Swiss bank. You will then need to make international transfers – either one-off or scheduled – to a French bank. However, this method is slower and more complicated, and you will incur unnecessary costs: bank charges, transfer fees, unfavourable exchange rates, commissions, etc.

• Or you could choose to open an account with an alternative online bank. These banks are more flexible and operate entirely online, offering significantly lower bank charges and more favourable exchange rates.

• Finally, you can use a currency exchange service that is better suited to the needs of cross-border workers to convert your CHF into EUR: it’s quicker and cheaper.

#1 To save yourself time-consuming administrative tasks

For many people, becoming a cross-border worker inevitably involves opening a bank account in Switzerland. Recognised as a leading financial centre, Switzerland benefits from excellent economic and monetary stability. Interest rates there are lower than in France, and can even be negative at times, depending on economic conditions. Swiss national banks also offer a wide range of banking products, which are popular with both Swiss residents and foreigners.

Despite this, as in most countries, a traditional Swiss bank account comes with a number of inconveniences that can be avoided.

Let’s take the example of opening an account at a bank in Geneva. Like any financial institution, the Swiss bank will ask its new customer to provide a range of supporting documents to verify the account opening:

- A valid form of identification (ID card, passport, driving licence, etc.)

- Proof of address dated within the last three months (water, electricity or gas bill, etc.)

- Your proof of income and/or proof of the source of your funds in the case of investments in Switzerland.

Documents will be systematically checked to verify their authenticity: either by the Swiss bank itself when they are submitted in branch, or in some cases by a notary if they are sent by post.

This verification process, known as due diligence, can take several days. But the wait doesn’t always end there: obtaining additional services, such as a credit card, may require further verification checks. To ensure your current account is fully operational, you’ll need to plan ahead for these procedures and be patient!

Exchange currencies easily and securely with b-sharpe

#2 To save on bank charges

Opening a bank account in Switzerland may seem reassuring, but the fees can quickly add up:

- Up to CHF 30 in management fees per month;

- Interbank transfer fees (processing of financial transactions);

- Fees for using in-branch banking services;

- Up to CHF 30 in debit/credit card fees per year;

- Commissions and currency conversion fees apply to every transaction.

All in all, they’ll cost you a lot of money without making your daily life as a cross-border worker any easier. So you can simply do without them, especially when there’s no need to open a bank account!

#3 How to stay true to minimalism

Juggling multiple accounts can be confusing, particularly when dealing with different currencies. What’s more, having several bank accounts makes tax management more complicated: for example, you’ll need to declare any interest earned on your Swiss account in your French tax return (even if it’s just a few francs).

Finally, some banks require a minimum deposit. Don’t be surprised if you’re required to maintain a minimum balance, or to carry out transactions regularly, or else face inactivity charges. Even basic current accounts are subject to these restrictions at some national banks

#4 To benefit from multi-currency solutions and more flexible international transfers

Being able to convert currencies quickly and transfer them at low cost shouldn’t be a luxury. That’s where innovative multi-currency solutions like b-sharpe come in. With this alternative, you can convert your CHF into EUR in just a few clicks, with no extra charges! You can even automate these transactions every time you receive your salary: managing two currencies has never been easier.

But that’s not all: the fees associated with these transactions are completely transparent, and the exchange rates are more competitive than those offered by domestic banks. This is yet another reason why multi-currency solutions are attracting growing interest from French residents.

In what situations can you manage without a Swiss bank account?

Avoiding unnecessary paperwork, avoiding various bank charges, keeping your finances flexible… There are plenty of reasons to do without a Swiss CHF account! Here are the two most common scenarios in which you won’t be required to open an account in Switzerland:

#1 Receiving your salary in Swiss francs or euros

As a French resident, working in Switzerland and receiving your salary in CHF does not mean you are required to open a Swiss bank account in order to transfer your salary into the currency of your choice.The solution is simple: b-sharpe provides you with a document to give to your Swiss employer, stating the reference code for your CHF account. This code, which your employer simply needs to include in the transfer reference, will allow you to be identified as the beneficiary.

The funds received will then be converted by b-sharpe at the best available rate as soon as they are received, and transferred within 24 hours to the beneficiary account of your choice, in the currency of your choice. This is a great option for any French resident looking for a quick Swiss franc to euro conversion.

#2 Converting currencies

To convert Swiss francs into euros (and vice versa), you don’t need to go through a Swiss bank account either. To get the best exchange rates without having to deal with a bank’s fees, the smartest option is to use a secure, fast and transparent multi-currency solution such as b-sharpe.

What are the options for managing your Swiss francs without a traditional Swiss bank account?

Opening a bank account in Switzerland will allow you to receive your salary directly in Swiss francs (CHF). You will then need to transfer it to your French account. However, there are smarter alternatives for working in Switzerland whilst living in France, without having to open a local bank account.

#1 Currency exchange services and personalised IBANs with b-sharpe

Online currency exchange services are the cheapest and most efficient alternative to traditional banks for managing salaries in foreign currencies. In practical terms, the b-sharpe platform allows you to receive funds via a Swiss personal IBAN, without having to open a bank account in Switzerland. The funds can then be converted into the currency of your choice before being transferred directly to your current account, in France or another country. Thanks to this IBAN, your employer can pay your salary quickly and easily.

These services also allow you to **save money on the “hidden” bank charges** that are all too often imposed by national banks. By bypassing these charges, b-sharpe offers transparent exchange rates and reduced fees on every transaction, without compromising on the speed of transfers… All this is delivered through an innovative and personalised service, tailored to the needs of cross-border workers!

#2 Bank accounts in France for international use

Generally speaking, cross-border workers do not close their French bank accounts so that they can continue to benefit from the advantages of the French banking system, such as fast, low-cost transfers to Switzerland, thanks to partnerships with Swiss banks. They also keep their regulated savings accounts (Livret A, LDDS), which offer favourable interest rates and tax advantages.

#3 Cross-border accounts in France with Swiss partners

Some local French banks, located in border areas, offer CHF and EUR accounts tailored to the needs of cross-border workers. This alternative to Swiss banks allows customers to deposit cash at their branches (in Swiss francs or euros). Even more appealing is the fact that this type of current account offers a preferential CHF/EUR exchange rate and allows customers to make transfers with an exchange rate guarantee.

Before opening a cross-border account with a French bank, please note that some Swiss employers require a Swiss IBAN for salary payments. You should therefore check this beforehand.

In this case, the closest alternative would be local Swiss banks located near the border, some of which offer CHF-EUR current accounts, known as “cross-border” accounts. Although specifically designed for this particular situation, Swiss cross-border accounts offer few additional features. They are essentially designed to receive your salary in Swiss francs (CHF) and transfer it to a French account in euros.

This solution remains a cost-effective and cheaper option than opening a standard current account in Switzerland to have your salary paid into in Swiss francs (CHF).

#4 Online banks

Online banks, also known as neobanks, are commonly used by cross-border workers. They can choose between a Swiss or French online bank.

These fully online banks offer a wide range of services accessible at any time via their user-friendly apps: credit and debit cards; multi-currency current accounts; simple international transfers; and more. This is a particularly useful service for cross-border workers who are far from their local branch.

Furthermore, some online banks offer free basic accounts and attractive referral schemes. In addition to lower bank charges, instant transfers are usually free, and the cost of international transfers remains competitive.

Some online banks even offer multi-currency accounts: these allow you to manage several accounts, in Swiss francs and euros, making it easier to convert currencies without incurring excessive fees.

The downside? The lack of human contact: they don’t have physical branches, which makes it more difficult to deposit cheques or cash. What’s more, their entirely digital customer service means it’s harder to speak to an advisor.

#5 Open a foreign currency account

A foreign currency account is an option that allows you to hold funds in the currency of your choice: euros, US dollars, Swiss francs, etc. It enables you to make transactions or transfers in these currencies without incurring any currency conversion fees.

For a cross-border worker, a foreign currency account offers several advantages. Firstly, it allows you to receive your salary in Swiss francs without incurring any conversion fees. A foreign currency account also makes it easier to spend money locally (in Switzerland) and when travelling abroad, without having to visit a currency exchange bureau.

Foreign currency accounts can be opened at traditional banks or online banks, each with their own terms and fees. Online banks often offer a simpler sign-up process and more competitive fees, but they may have a more limited range of available currencies.

Why a cross-border worker’s income depends on the EUR/CHF exchange rate

Cross-border workers in Switzerland are often paid in Swiss francs (CHF) but have to cover their expenses in euros (EUR) in France. However, for cross-border workers, converting their salary from Swiss francs to euros is a recurring issue. They have to do this every month and are heavily dependent on the prevailing exchange rate. Their purchasing power and the final amount of their salary are directly influenced by the EUR/CHF exchange rate.

A cross-border worker’s income is exposed to exchange rate risk, which is directly influenced by fluctuations in the exchange rate between the euro and the Swiss franc. Thus, when the Swiss franc is strong, cross-border workers enjoy greater purchasing power in France, as their converted income is worth more in euros. Conversely, when the euro is strong, their purchasing power is reduced, as each converted Swiss franc yields fewer euros.

The cost of living in Switzerland is actually higher than in France. Currency exchange services such as b-sharpe allow you to make the most of these fluctuations without having to constantly monitor the exchange rate.

💡 Converting your Swiss francs into euros is now easy!

Using a currency converter, such as b-sharpe, allows you to benefit from a more favourable exchange rate compared to traditional providers.

The rate offered for an EUR-CHF or CHF-EUR conversion is therefore much lower than at a traditional bank.

#6 Ethical and sustainable banks (Swiss Alternative Bank – BAS)

To remain true to their values, French residents can also opt for an alternative bank account based in Switzerland. To this end, institutions such as the Banque Alternative Suisse (BAS), which has branches in Geneva, Lausanne and Zurich, operate on a cooperative and transparent model. This is a conscious choice to help fund social or environmental projects.

These alternative Swiss banks cater to both Swiss residents and cross-border workers. Some institutions also offer temporary accounts, with no long-term commitment, for receiving a salary in CHF before converting it to EUR. Known as ‘free transfer accounts’, this option is available only to workers who have already contributed to the Swiss pension system. This option allows you to retain a Swiss IBAN for a short period.

Finally, alternative banks offer additional products for cross-border workers wishing to become Swiss residents. These include, for example, pillar accounts for long-term savings, or rent guarantee schemes that meet the requirements of certain Swiss building societies. Although they do not always include a credit card as part of their basic package, they can easily be combined with a neobank or a multi-currency account such as b-sharpe to keep costs down.

Why a cross-border worker’s income depends on the EUR/CHF exchange rate

A French resident paid in Swiss francs (CHF) generally covers most of their expenses in euros (EUR) whilst in France. To do so, they therefore convert their CHF into EUR every month, either in full or in part. Although this is a regular transaction, it is never cost-neutral. As it is constantly subject to exchange rate fluctuations, the value of their final income either increases or decreases each month.

As wages and the cost of living in Switzerland are significantly higher, French cross-border workers enjoy greater purchasing power on average. Furthermore, when the Swiss franc appreciates, their purchasing power increases. However, when the euro is strong, their purchasing power is reduced, as each Swiss franc converted yields fewer euros.

To counteract this effect, currency exchange services such as b-sharpe allow you to make the most of these fluctuations without having to constantly monitor exchange rates. Using a currency converter enables you to benefit from a more favourable exchange rate compared to traditional providers. The rate offered for an EUR-CHF or CHF-EUR conversion is therefore significantly lower than that of a traditional bank.

How do you choose the best option for your situation?

The choice of an alternative to opening a Swiss bank account will depend on several factors:

- Your status: cross-border worker, temporary expatriate, French or Swiss resident.

- The frequency of money transfers between Switzerland and France.

- Your requirements regarding currency exchange or additional banking products (cards, loans, investments, etc.).

- Simplicity, the range of services on offer, or your commitment to ethical values.

For example, a cross-border worker looking to maximise their purchasing power would be best advised to use a currency exchange service with a Swiss IBAN, whereas a French national wishing to become a Swiss resident could opt directly for a Swiss bank in order to access country-specific products, such as pillar accounts (retirement savings) or rent guarantee accounts.

Why choose b-sharpe as an alternative?

b-sharpe’s commitment: to enable everyone to manage their Swiss francs and euros with complete freedom, without the hidden costs or constraints of traditional banks.

Recognised as a leader in currency exchange, b-sharpe offers a personal Swiss IBAN and competitive exchange rates. With its attentive local team, secure and fast transfers, b-sharpe is the smartest solution for managing two currencies with ease, without losing out on exchange rates!

Frequently asked questions about alternatives to Swiss bank accounts

Yes, thanks to platforms specialising in currency exchange such as b-sharpe. It is now possible to receive your salary in Swiss francs (CHF) into a Swiss personal IBAN account without opening a traditional bank account in Switzerland. This allows you to avoid lengthy account opening procedures, whilst benefiting from more favourable exchange rates and lower fees when converting your CHF to EUR.

Some employers require a Swiss IBAN to make salary transfers, even if you are a French resident. In this case, you can opt for:

• A currency exchange service with a Swiss IBAN, such as b-sharpe;

• A CHF-EUR account for cross-border workers, offered by certain French or Swiss banks, usually located near the border.

Important: before choosing an alternative solution, check carefully which IBAN formats are accepted by your employer.

The Swiss National Bank sometimes applies negative interest rates. This policy results in a cost on deposits at certain banks, even on current accounts (particularly for large sums).

Here are the alternatives to avoid them:

• Opt for currency exchange services that do not hold your funds. They thus carry out the conversion and transfer immediately to your French account.

• Opt for online banks or multi-currency accounts that do not impose this type of penalty.

• Split your deposits if you hold large sums.

Alternative Swiss banks generally offer more flexible terms than the major Swiss national banks, but it is always advisable to read the interest terms carefully.

Did you know that some banks offer the option to fix the exchange rate? This allows you to benefit from a favourable rate for longer and means you no longer have to worry about fluctuations in the Swiss franc exchange rate. But is fixing the exchange rate a good idea? b-sharpe explains everything in this article!

The exchange rate of the Swiss franc

What is the exchange rate for the Swiss franc? As you are no doubt aware, exchange rates – including that of the Swiss franc – are constantly changing. They fluctuate on a daily basis on the Forex market. There are many factors that cause the Swiss franc, and all other currencies, to fluctuate:

- The specified period

- The economic climate

- Monetary policy pursued by central banks

- Investor reaction

- The price of energy resources…

But how can you tell whether an exchange rate is favourable or not? To find out whether the exchange rate you’ve been offered is favourable – and thus determine whether the margin charged by your financial intermediary is too high – you can compare it to the reference rate (or ‘interbank rate’). This is the rate at which banks trade with one another. You can find it on all financial data websites.

With innovative financial intermediaries, you can exchange currencies online and benefit from competitive exchange rates compared to those offered by traditional providers such as banks or currency exchange bureaux.

How to lock in the Swiss franc exchange rate: the forward contract

For all your financial transactions between France and Switzerland (transferring your salary, making bank transfers, etc.), you need to take the exchange rate into account and find the best time to make your transfers, so as not to lose out on the exchange rate. Some people have decided to opt for a fixed exchange rate. This is known as a forward sale.

What exactly is a futures contract?

A forward sale is a contract entered into between an individual and a bank. It allows the exchange rate to be fixed at a rate that will apply to all currency conversions for a specified period. This period is usually set at 3, 6 or 12 months. Thus, when converting Swiss francs into euros, a forward sale commits the customer to selling a certain amount of Swiss francs to their bank each month in exchange for a certain amount of euros, at the rate specified in the contract.

Fixing your Swiss exchange rate: pros and cons

At first glance, fixing the exchange rate seems very advantageous. In particular, it allows you to benefit from a favourable rate for longer and means you no longer have to worry about fluctuations in the Swiss franc exchange rate. For an individual, this therefore provides protection against any unfavourable changes in the exchange rate. They no longer need to monitor exchange rates or look for the best time to carry out their transactions, as their bank handles the conversion.

However, this process has undeniable drawbacks. Firstly, the individual agrees a rate with their bank and will therefore be unable to benefit from a more favourable rate should market conditions improve. Furthermore, fixing the rate comes at a cost: the bank charges an administration fee and applies a margin on transactions that can sometimes be substantial. Finally, the bank may charge fees and penalties if you do not pay your salary into the account by the agreed deadline. With a forward sale, the customer is contractually obliged to make monthly payments to their bank. However, if life’s uncertainties (financial difficulties, unexpected expenses, redundancy) prevent them from paying the amounts due, the bank may claim penalty charges. Fixing the exchange rate therefore presents a financial risk that should not be overlooked.

b-sharpe, an alternative to exchange rate pegging in Switzerland

Fortunately, there are other ways to take advantage of a favourable exchange rate for all your currency conversions without having to lock in a rate (or use forward sales). b-sharpe, an online currency converter, offers you a cost-effective, user-friendly, fast and secure solution for all your currency exchanges, with reduced exchange fees.

A reliable and secure online currency converter

b-sharpe customers can lock in their exchange rate in real time and have 48 hours to complete their transaction.

Monitor rates with alerts

With b-sharpe, receive alerts when your currencies reach your desired exchange rate, and track the movements of more than 20 currencies. Set up exchange rate alerts in your customer portal and be notified at the best time to carry out your transactions.

How does b-sharpe’s CHF/EUR currency exchange service work?

The b-sharpe currency converter stands out for its ease of use! It takes just three steps to convert your Swiss francs into euros.

- Set up the transaction in your b-sharpe customer portal: provide details of your transaction and specify the amount you wish to exchange in the target currency, as well as the account into which the funds will be paid.

- Sending funds to b-sharpe from your bank account: using your banking app, make a bank transfer to b-sharpe’s IBAN, which you can download from your customer portal or find in your exchange confirmation

- b-sharpe processes the transfer in the target currency: as soon as we receive your funds, they will be converted and sent to the recipient’s account!

With an innovative, 100% online service, b-sharpe is your go-to partner for all your euro-to-Swiss franc transactions or dollar-to-Swiss franc conversions.

b-sharpe’s currency exchange glossary!Bank

Version 4.0 of the Swiss banking system, a mainstay of the Swiss economy. It comprises investment banks, private banks, industrial and commercial banks, and even ‘non-bank banks’ (i.e. large retailers which, driven by shrinking profit margins, sell financial products). Not to mention the latest addition: online banking!

A bank is therefore a business that provides and trades in banking and other financial services. It lies at the heart of the financial sector and is directly responsible for managing financial risks. It can handle your foreign exchange and credit transactions… depending on the rates and terms, which you should compare carefully!

ECB

The European Central Bank (ECB) is the central bank of the nineteen European Union countries that have adopted the euro. It is the European Union’s main monetary institution.

Not to be confused with the Banque Commune d’Épreuves! Although its main remit could be seen as a challenge: maintaining price stability in the eurozone, and thereby preserving the purchasing power of the single currency for all the member states concerned.

SNB

The Swiss National Bank (SNB) is Switzerland’s central bank.

The SNB is a public limited company, though it is not really one in the strict sense of the term, in that no one is supposed to be unaware of either its existence or its remit:

- The SNB ensures the stability of the Swiss franc by drawing on its gold reserves and its foreign exchange reserves;

- The SNB manages the accounts that the Confederation has opened with the bank for the purpose of making payments;

- The SNB issues federal government bonds;

- The SNB advises the Swiss Confederation on where to invest its funds on a temporary basis.

Currency exchange

Currency exchange bureaux are financial intermediaries whose main business is manual currency exchange, i.e. the immediate exchange of one currency for another. As traders dealing in banknotes, they are subject to specific rules and must clearly display their rates and terms of sale (exchange rates, commission or any charges). A currency exchange bureau purchases its currencies and, depending on the balance between supply and demand, determines the selling rate and the buying rate for the currency.

Indexation clause

In the case of an international foreign exchange settlement agreement, the contracting parties may include an indexation clause designed to set out in the contract how the foreign exchange risk associated with the transaction is to be shared between the buyer and the seller.

It provides for compensation in the event of a fluctuation in the exchange rate of the currency chosen by the parties. Thus, the price may be adjusted automatically to protect against the risk of currency depreciation: a clause indexing the price to the value of gold (gold-backing clause) or to the exchange rate of a foreign currency (exchange rate guarantee).

Deadline

The specific time by which a transaction must be completed. This is the time by which payment orders must be submitted in order to be processed on the same day. These procedures ensure that transactions are allocated consistently when the accounts are closed at the end of each financial year. Right then… Cut. That’s enough said!

Today’s rates

Set daily, a currency’s daily exchange rate is the value of that currency relative to another on a given day. Quoted on the foreign exchange market, known as ‘Forex’, exchange rates fluctuate constantly depending on trading activity. The exchange rate is determined by supply and demand: if demand for the first currency exceeds supply, then its value rises relative to the second. In short: a constant balance of power!

Currency hedging

Hedging is a practice that involves protecting oneself against an unwanted risk. It is used by both manufacturers (who seek to protect themselves against fluctuations in the capital markets) and investors in the financial markets.

For a private individual, a foreign exchange hedge is a binding contract with their bank that allows them to lock in the exchange rate between two currencies at the time the transaction is concluded. The rate is fixed for a future date, for a specified amount.

A word of advice: check your cover, as you might get cold feet and want to switch 😉

You may also want to read our guide to futures trading for private individuals.

Value date

The date on which a particular banking transaction is recorded. In the case of a foreign exchange transaction, this is the date on which the currencies will be credited to the account. This is referred to as the spot value date, which corresponds to the date of delivery of the currencies for a spot foreign exchange transaction. This should be distinguished from the transaction date, which corresponds to the date on which the transaction is recorded. The two may differ by one or more days.

However, when calculating debit or credit interest, the value date is taken into account…

Currency

A currency accepted by a foreign country. The ‘currency’ is that of one’s own country.

Direct debit

Option to have the amount debited directly from your account. The account holder (debtor) authorises the issuer of an invoice (creditor) to debit the amount due directly from their bank account for payment.

FED

The Federal Reserve System, or the Fed. Contrary to popular belief, the Federal Reserve is indeed the central bank of the United States (and not a nickname for the tennis player from Basel).

The US Federal Reserve has a dual mandate to ensure price stability whilst supporting employment. As the body responsible for monetary policy – notably through setting key interest rates, and thus the cost of borrowing – the Fed closely monitors the economy to prevent it from overheating: inflation, unemployment, domestic and external growth…

Figure

In forex jargon, these are the first three digits of a buy or sell quote for a currency pair. For a spot EUR/USD quote of 1.2530/40, for example, the figure is 1.25. For the sake of speed, currency traders refer only to the pips, i.e. the last two digits of the 54 to 65 significant digits quoted in a ‘calm’ market and for a ‘non-exotic’ currency. Thus, if the rate moves from 1.25 to 1.26, we say it has risen by one pip.

Forex

An abbreviation often used to refer to Foreign Exchange, i.e. the global currency market. The foreign exchange market is a decentralised global market that determines the relative values of different currencies. It generally refers to the trading activities of investors and speculators in the foreign exchange market.

Unlike other markets, there is no centralised exchange or clearing house through which transactions are conducted. Transactions are carried out over-the-counter. You can buy or sell any currency pair at any time, subject to available liquidity. There is no ‘seller’s market’ in the traditional sense of the term. You can make (or lose) money, whether the market is trending upwards or downwards.

Forward

Means ‘forward’ in English. An over-the-counter technique that allows a rate to be fixed in advance.

IBAN

International Bank Account Number: an international bank account number that complies with the ISO international standard.

Consisting of 21 characters for Switzerland: 4 characters (2 letters for the country and 2 digits), followed by the bank identifier (SWIFT or BIC) and the account number. It facilitates transactions between economic operators in the eurozone and contributes to the development of trade.

Spot market

A market in which the purchase and sale of financial assets are settled and delivered on T+2, unlike deferred settlement transactions or the futures market. In a spot market, the spot price is therefore used to determine the value of the transaction. The investor must hold the assets required to settle the orders placed in order for the transaction to take place.

Futures market

A market in which transactions involve payment and delivery at a future date. The flagship product of these markets, the futures contract, is an agreement whereby a buyer undertakes to purchase from the seller all manner of assets: currencies, interest rates, and mineral, agricultural or energy commodities. All of this takes place at a specified future date.

Unlike forward contracts (traded on over-the-counter markets), the terms of futures contracts are standardised: the quality of the deliverable commodity, the quantity or trading unit, the expiry dates and the delivery terms are all fixed in advance. Only the price is negotiated by the traders.

Margin

You don’t need to watch *The Wolf of Wall Street* and its famous “sell me this pen!” scene to understand that margin is a key indicator in any commercial or banking transaction.

Strictly speaking, it is defined as the difference between the selling price and the purchase price. The margin may relate to a purchased item (goods), a manufactured item (product) or a service (provision of services), as in the case of a foreign exchange transaction, for example.

NDF (non-deliverable forward)

When a currency is not deliverable. This is an instrument designed to hedge currency risk for currencies where access to a forward foreign exchange market is (very) restricted, or even prohibited for non-residents. In principle, an NDF is equivalent to a forward exchange contract, except that at maturity there will be no delivery of the local currency.

Designed to hedge currency risk for currencies that cannot be traded on the conventional forward market, the convertible currency is usually the US dollar, although it is possible to trade against the euro, Swiss franc, pound sterling, etc. A ‘non-deliverable forward’ contract is for a fixed amount in the local currency.

The counterparties agree on a maturity date, a forward exchange rate and the method for determining the reference rate (at maturity).

Forward transaction

A firm contract between the bank and its customer, which allows the customer to lock in, at the time the transaction is concluded, the exchange rate of one currency against another, for a specified amount, at a future date.

A forward contract allows the client to lock in and guarantee, at the time the contract is concluded and without paying a premium, a buy/sell rate for their currency for a transaction with a fixed maturity date and amount.

It allows a company to hedge the foreign exchange risk associated with a commercial transaction involving foreign currency. The company thus knows the exchange rate at which it will sell or buy the currency in the future. The rate is fixed, regardless of the currency’s market rate at maturity. The company cannot benefit from any favourable movements in the currency’s value.

Currency exchange option

A foreign exchange option is a contract that gives the buyer the right (but not the obligation) to buy or sell a specified amount of foreign currency on a specified date (or during a specified period) at a predetermined exchange rate known as the strike price, in return for the payment of a premium.

Parity

In the Forex market, it indicates the exact point at which two currencies are of equal value: the exchange rate between these two currencies is 1. This concept is also used in options, where the value of an option is equal to its intrinsic value.

Pips

This is the unit of measurement for changes in the exchange rate (of a currency pair) in points. In practical terms, it refers to the last two digits of a quote, out of the four or five significant digits given in a foreign exchange market. In our example of a quote of 1.2530/40 for EUR/USD, the pips are 30/40.

Bank details

Commonly known as a bank account number. A sort of banking barcode, just as well-known as its counterpart, the PIN: it helps to streamline transactions and reduce transaction costs by standardising account numbers and the details of banking transactions.

Why? Because there are as many types of transactions and accounts as there are regional specialities … So it’s just as important to be able to provide your bank details as it is to give your mobile number. You get the picture.

Currency risk

Currency risk refers to fluctuations in exchange rates that may affect the profitability of an investment.

SEPA

“Single Euro Payments Area”, literally “single euro payments area”. It was established by the member banks of the European Payments Council to harmonise euro payment methods across member countries, which include the countries of the European Union, Monaco, Liechtenstein, … and Switzerland.

SEPA covers credit transfers, direct debits and the use of bank cards. In practical terms, this enables users (consumers, businesses, merchants and public authorities) to make payments in euros under the same conditions throughout the European Economic Area, just as easily as they would in their own country.

SPOT (spot market)

The term ‘spot rate’ refers to the current rate applicable to an immediate transaction. The spot rate is distinct from the forward rate.

Spread

Refers to a spread (usually between the bid and ask prices). If we take the example of an EUR/USD quote of 1.25 {30} / {40}, the difference between the ‘bid’ (i.e. the price at which the dealer buys) and the ‘ask’ (i.e. the price at which the dealer sells) is called the spread.

The spread, which is determined by the broker, is set based on the transaction amount, market volatility and market sentiment.

SWAP

Derivative financial product. It involves the exchange of debt instruments or different currencies on different terms (at a fixed or variable interest rate) in different countries.

Swaps are contracts for the exchange of cash flows:

- That is, interest rate swaps: transactions involving loans.

- That is, foreign exchange swaps: contracts for the exchange of currencies.

Currency swap

A financial transaction in which two parties agree to exchange currencies today at the spot exchange rate and to exchange the same currencies at the contract’s maturity date at the forward exchange rate. No interest is exchanged; only currencies are exchanged at the start and end of the swap, which has a term of less than one year.

Currency swaps

In the over-the-counter market, over the longer term: these are transactions involving financing terms. The aim is to diversify and thus optimise the loan portfolios of banks and businesses.

Not to be confused with:

- the blogosphere swap (gift exchanges between internet users based on a theme, for example swapping slimming products for cookbooks);

- the wrap (even though ‘the better the operation is organised, the more satisfaction it will bring you’);

- swag (someone who is stylish and charismatic). The only thing they have in common is that any self-respecting swag must follow the rules of ‘swagitude’, which, by definition, vary from country to country and with changing fashions.

SWIFT

An acronym for the Society for Worldwide Interbank Financial Telecommunication. Originally established as a banking cooperative, it now provides standardised interbank messaging services and interfaces to more than 10,800 institutions in over 205 countries.

The organisation manages the registration of BIC codes. This is why the term ‘SWIFT code’ is sometimes used to refer to the BIC, which is linked to the IBAN. The SWIFT code identifies a bank; it consists of a country code, a bank code, a code to locate the bank and, finally, a code to identify the branch. E.g.: BCGECHGGXXX.

Exchange rates

The rate (i.e. the price) at which one currency can be bought or sold in exchange for another. As it is floating, the exchange rate is determined at each transaction by the balance between supply and demand on the foreign exchange markets. It is then traded either at the spot rate (generally within two working days) or at a forward rate, at a future maturity date.

Interbank exchange rate

The interbank exchange rate is the real-time rate at which banks trade currencies with one another on the interbank market, a market reserved for banks.

Minimum rate

Set by the SNB in 2011 at 1.20 francs to the euro, the exchange rate floor was intended to counter the appreciation of the franc and protect exports by Swiss SMEs. It was abandoned in January 2015 because the mass purchase of euros was no longer sustainable for the institution.

5 things you need to know about the EUR/CHF exchange rateWhilst it isn’t necessary to understand all the intricacies of the foreign exchange market to carry out currency transactions, a better understanding can nevertheless help you optimise the way you exchange your Swiss francs by securing a better exchange rate. Discover the 5 key factors that influence the euro-Swiss franc exchange rate.

#1 The EUR/CHF exchange rate is determined by supply and demand

The Swiss franc and the euro are so-called ‘floating’ currencies: this means that the two currencies are traded at a variable rate, determined by the laws of the foreign exchange market. Supply and demand are therefore the two factors that cause the exchange rate to fluctuate.

Let us suppose, for example, that the EUR/CHF exchange rate is 1.10 (i.e. it costs 1.10 CHF to buy 1€ at time t) and that the market starts selling large quantities of euros against all other currencies at time t+1. The price of the euro will then fall, which will relatively strengthen the Swiss franc in the EUR/CHF pair. The value of one euro will then be less than 1.10 CHF.

We can therefore draw two conclusions from these observations on the EUR/CHF exchange rate:

- When there are more sellers than buyers, the price falls.

- When there are fewer sellers than buyers, the price rises.

#2 The EUR/CHF exchange rate is constantly changing

It is important to understand that the EUR/CHF exchange rate fluctuates constantly. Consequently, it will usually be impossible to compare the EUR/CHF exchange rate accurately between different financial institutions.

This is because the euro-to-Swiss franc exchange rate displayed by financial institutions and bureaux de change is generally not the real-time exchange rate, but the daily rate.

To get the latest exchange rate and minimise currency risk, the best option is still to use a real-time EUR/CHF converter such as the one provided by b-sharpe.

#3 The EUR/CHF exchange rate quoted by financial intermediaries includes various margins

The EUR/CHF exchange rate offered by bureaux de change, banks or online currency exchange services may vary from one provider to another. Why is this? Simply because each financial intermediary applies what is known as a margin, which represents their fee.

The margin is expressed as a percentage of the amount exchanged. It varies depending on the financial intermediaries involved. This margin is undoubtedly an important factor to consider when choosing a financial intermediary, as it is deducted directly from the amount you exchange!

When exchanging Swiss francs for euros, the margins may vary:

- Banks generally offer the highest margins (between 1.65% and 1.70% for amounts under CHF 10,000);

- currency exchange bureaux charge a mark-up (ranging from 0.65% to 2%);

- Online currency exchange services offer the lowest spreads (around 0.50%).

The size of the organisation, the number of intermediaries involved in the transaction and the level of digitalisation of services are all factors that affect the costs borne by each of these parties. These structural costs are reflected in the margins and are ultimately passed on directly to your wallet!

The best option is therefore to choose a structure:

- small or moderate in size;

- with as few intermediaries as possible;

- which offers a digital solution.

This helps to explain the rise and success of online currency exchange services such as b-sharpe, which ultimately offer the most competitive Swiss franc–euro exchange rates, including all margins.

#4 Swiss SMEs are being affected by the rise in the value of the Swiss franc against the euro

In January 2015, the SNB (Swiss National Bank) abandoned the EUR/CHF exchange rate floor. This move allowed the Swiss franc to appreciate rapidly and significantly against the euro.

Contrary to appearances, the appreciation of the Swiss franc – which makes it a strong currency – is clearly not good news for the Swiss economy in the long run! Indeed, half of the wealth created in Switzerland (GNP) comes from exports.

In other words, the surge in the value of the Swiss franc against the euro is pushing up export prices. Some Swiss companies are immediately losing ground in terms of competitiveness compared with their main trading partners in the eurozone, and SMEs are the first to suffer…

#5 Currency risk can arise at various levels

Faced with the latent exchange rate risk between the Swiss franc and the euro, some Swiss SMEs and large companies are choosing to invoice their goods and services not in Swiss francs, but in their customers’ currency: the euro.

Whilst, on the face of it, such a measure allows a company to maintain the same pricing and remain competitive, the risk lies elsewhere. By receiving payments in euros without adjusting its prices, the exporting company exposes itself to exchange rate risk.

Conversely, importing companies will be able to benefit from the appreciation of the Swiss franc by taking advantage of more affordable invoicing in a ‘weak’ euro. To manage this exchange rate risk, which always affects one party or the other, forward contracts allow the parties to agree on a fixed exchange rate that suits both signatories.

You are now fully aware of the ins and outs of the Swiss franc-euro exchange rate. Despite all these factors, there are simple solutions to optimise the Swiss franc-euro exchange rate!

#1 Transfer your CHF to France directly from your Swiss bank account

Some of you have probably already tried transferring your Swiss francs directly into your French euro account. Whilst this may seem the simplest and quickest option, it isn’t always the best solution.

Transferring CHF to your EUR account involves making an expensive international transfer. As a reminder, an international transfer involves transferring funds from a bank account in one country to a bank account in another country. This can be done between bank accounts held in the same currency or in different currencies.

If you wish to transfer your Swiss francs from a Swiss bank to a euro account at a French bank, the international transfer will involve a currency conversion, as the currency of the transfer is not the same as that of the recipient account. Your bank in France will automatically convert your Swiss francs into euros upon receipt of the funds. This will therefore incur currency conversion fees that are beyond your control, and you are likely to be offered an unfavourable CHF/EUR exchange rate.

However, with an online currency exchange service such as b-sharpe, the transaction will be processed at the best rates, regardless of the destination. Once your bank transfer in Swiss francs has been made, the funds will be credited to your French bank account within two working days on average.

#2 Choosing a bank because it operates in Switzerland and another country

The argument for an international presence carries significant weight when looking for a CHF–EUR currency exchange solution.

However, the physical location of your bank comes at a cost that inevitably affects other overburdened services such as:

- credit card;

- the exchange rate margin;

- account maintenance fees;

- and many other committees.

This conversion, which might seem free, actually involves very real costs. And as these institutions do not disclose their exchange rate margins, it is impossible to quantify the actual financial benefit to you.

#3 Using a bank for CHF-EUR currency exchange

As currency exchange specialists based in Geneva, we have realised that your needs and expectations are not being met by banks that generate more than 25% of their profits from foreign exchange transactions.

Nowadays, banks are no longer able to offer truly competitive and transparent services to their foreign exchange customers. Currency exchange bureaux, for their part, have their own limitations.

Your bank may charge a spread of up to 1.65% (compared with just 0.50% at b-sharpe), not to mention currency conversion fees and the fact that the availability of advisors can leave something to be desired.

Whether you’re an individual or a business, our team of foreign exchange and trading specialists is on hand to answer your questions via chat, phone or email.

#4 Repaying your mortgage in foreign currency and exchanging currency through your bank

You don’t have to go through your bank for currency exchange when repaying a mortgage. As with any other currency exchange transaction, online currency exchange services can be advantageous.

Once your flat has been sold, if your mortgage is denominated in a foreign currency (and secured by a deposit), the proceeds of the sale (in euros) will be paid into a euro-denominated account.

From there, b-sharpe converts the euros into Swiss francs and transfers the Swiss francs to your account, so that you can repay the loan to your bank.

#5 Trading on margin as a private individual

On the face of it, a forward sale might seem like a good idea: every month, your bank buys Swiss francs on your behalf and converts them into euros at a rate fixed in advance for a set period (from 3 to 12 months). You know exactly how much your budget will be, regardless of exchange rate fluctuations or economic upheavals resulting from potential political changes.

However, security comes at a high cost: the bank charges you for the absence of exchange rate risk offered by forward contracts via a substantial margin, on top of the administrative fees. The cost of this protection is built into the contract through a fixed exchange rate that is not particularly favourable compared to the rate you would get if you carried out your foreign exchange transaction on a spot basis.

When the unexpected happens, a forward sale is not synonymous with flexibility. An unforeseen event, such as the termination of your employment contract, can bring an end to the forward sale agreement you have entered into with your bank. The early termination of such an agreement generally entails high costs.

Fair enough, you might say? Yes and no. What about the penalties that apply if you decide to terminate the contract? The further the exchange rate on the date the contract is terminated (or spot rate) is from the forward rate, the higher the penalties will be.

What is a safe-haven asset?The best known: gold

When you hear the term ‘safe haven’, even if you’re not involved in the world of finance, the asset most often mentioned is gold. Whenever there is instability in the world, gold is highly sought after because it acts as a safe investment, unlike financial investments such as shares. It is also unaffected by low or high interest rates. Gold is also very easy to sell, whether in the industrial sector or in jewellery, and supply is limited. The precious yellow metal reached an all-time high in 2020, with the price exceeding $2,000 per ounce.

The strength of the Swiss franc

The Swiss franc has always been a safe-haven currency, particularly when market instability arises. The currency’s main strengths lie in the robustness of the banking sector and the country’s thriving economy. Added to this is a very low level of debt compared to other OECD members and persistently low unemployment. Furthermore, its independence from the surrounding European Union adds an extra layer of appeal as a safe haven for capital, particularly when the EU is facing the full brunt of economic, political and health-related challenges.

Government bonds

A government bond is simply a debt instrument issued by a government that provides for interest payments. Government bonds from developed countries (particularly G10 members) are also highly sought after during times of instability, as the risk of government default remains minimal.

Is the yen a safer bet than the US dollar?

The Japanese currency has long been a safe-haven asset, arguably even more so than the US dollar, given that the yen tends to appreciate more than the US dollar during periods of instability. This reputation stems from Japan’s large trade surplus relative to its debt throughout the 20th century. Nevertheless, Japan’s public debt is the highest in the world, accounting for over 200% of Japanese GDP. Despite this, the yen remains a safe haven, as Japan remains a powerful economy and over 90% of the public debt is held by Japanese companies and households, which provides a degree of stability.

The US dollar, the most liquid currency

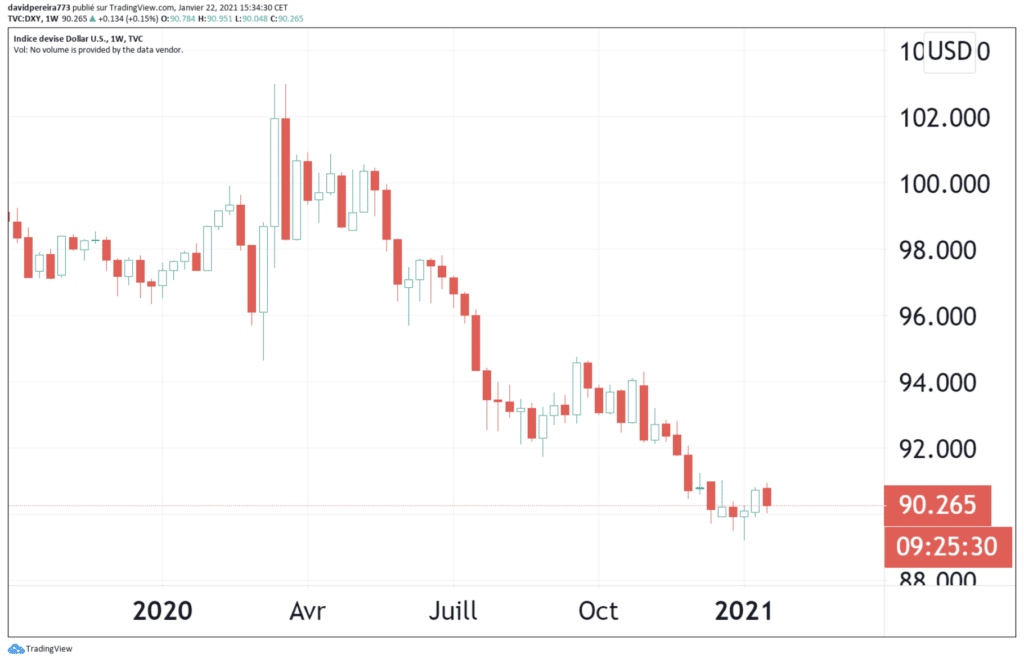

This confidence arose in the wake of the Bretton Woods agreements, which established a fixed exchange rate and effectively propelled the US dollar to become the world’s leading reserve currency. Then came the emerging market crisis of the 2000s, which further boosted the dollar’s value. Furthermore, the dollar is the most liquid currency in the foreign exchange market and simply symbolises the world’s largest economy today. However, the greenback is no longer considered a safe haven, and 2020 was likely proof of this. The DXY index, which is the benchmark index for the greenback against six major currencies—including the euro, which accounts for 57% of the total weighting—was shaken during this period. After rising to 103 in March 2020, the greenback’s strength has continued to fall throughout the pandemic, reaching as low as 89.20 in early January 2021.

Chart of the DXY index on 22 January 2021

Cryptocurrencies

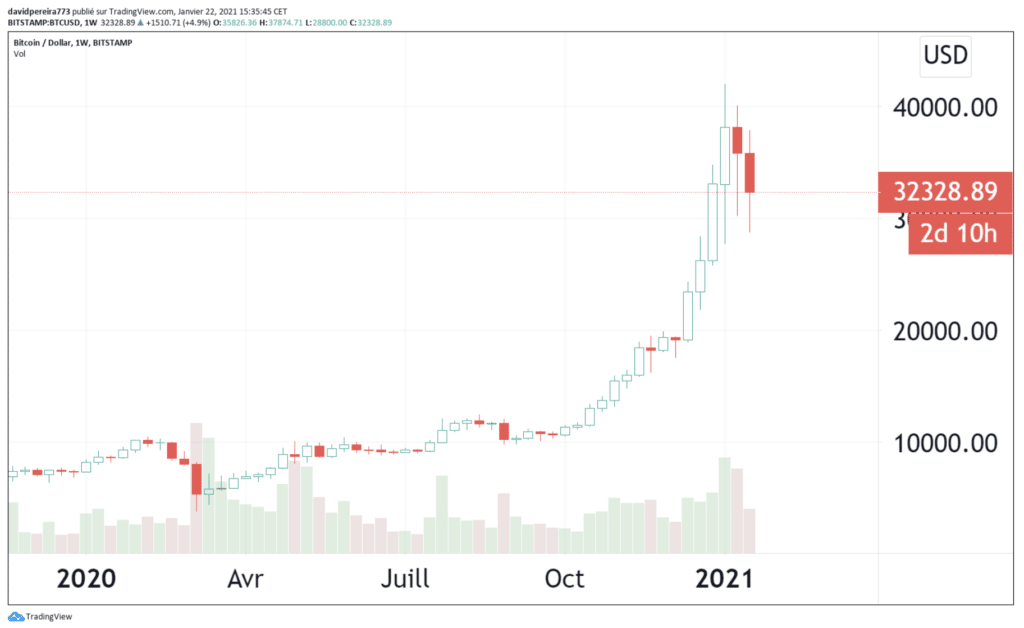

We are going to look at cryptocurrency, and more specifically at Bitcoin, which has been cited during this crisis as a kind of safe haven. Just like gold, Bitcoin is completely independent of politics and stock markets. However, its extreme volatility (up to +40% in a single day) has so far undermined the notion that it is a safe investment. As you can see below, Bitcoin has continued to rise in value since the start of the year, particularly during the first and second waves of COVID. We must not overlook the fact that the US dollar has depreciated, making dollar-denominated financial instruments more accessible (cheaper).

Bitcoin chart on 22 January 2021

One final interesting point to note during this health crisis is that technology stocks (GAFAM, Netflix and Tesla) experienced a significant surge and were regarded as safe-haven assets during the first wave of the coronavirus. Their market capitalisation rose exponentially, reaching a point in April 2020 where they accounted for 50% of the total value of the Nasdaq index.

To sum up, 2020 was a particularly surprising year, and it has likely put an end to the US dollar’s appeal when the market is in risk-off mode. Conversely, new assets such as tech stocks and Bitcoin have fared well. The question remains, however, as to whether this type of financial instrument could become the new safe-haven assets, or whether we should simply consider 2020 to have been a one-off.

Everything you need to know about exchange rates1 – What is the interbank exchange rate?

The interbank rate essentially reflects the value of one currency against another when two banks exchange them. This rate fluctuates constantly in line with the law of supply and demand.

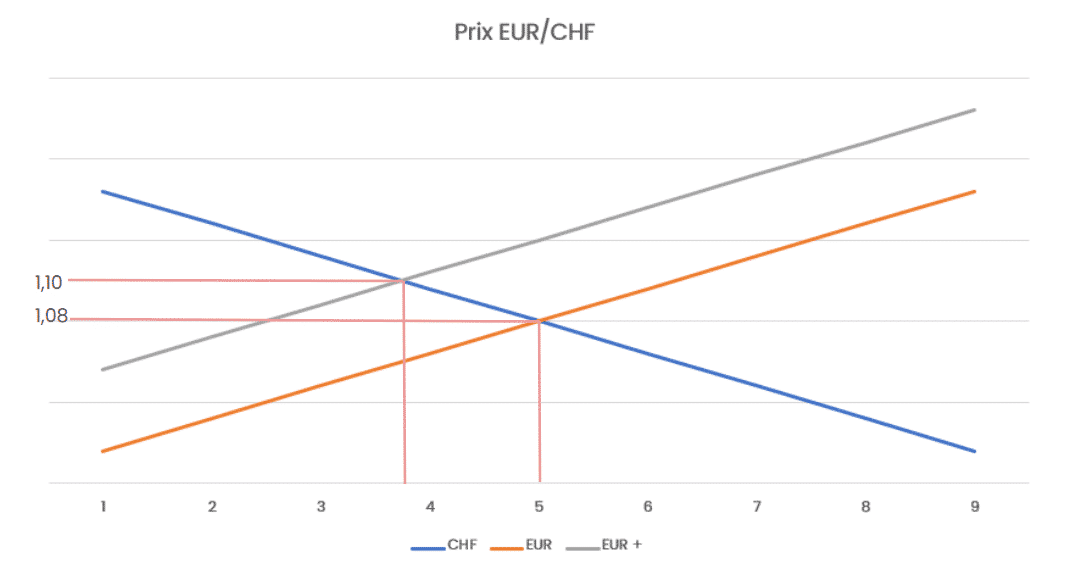

For example, when we talk about EUR/CHF, we are referring to the exchange rate or interbank rate between the euro and the Swiss franc. In this case, if the interbank rate is 1.10, this means that for one euro, the market will pay you 1.10 francs.

As this market is based on supply and demand, this means that it will fluctuate depending on the number of buyers and sellers.

For example, if the banks (and market participants through them) decide to buy large amounts of euros in exchange for francs, the exchange rate will rise. In other words, for one euro, you will no longer get 1.08 CHF but 1.10 CHF.

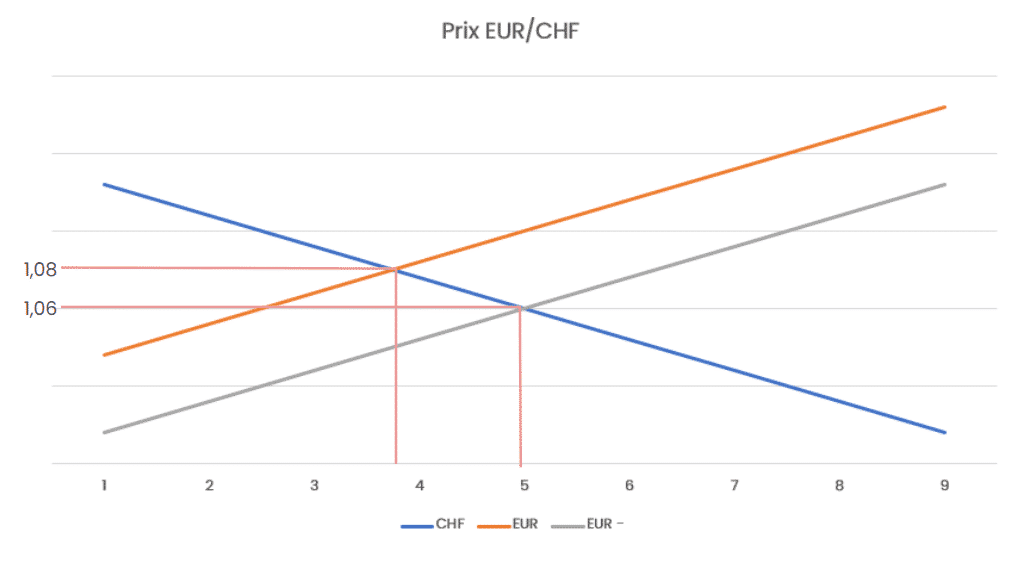

Conversely, if there are many sellers of the euro, the EUR/CHF exchange rate will fall; in other words, for one euro you will no longer get 1.08 CHF but 1.06 CHF. The price is therefore a compromise between the sellers and buyers of a currency and is governed by the laws of supply and demand.

The number of buyers or sellers fluctuates constantly. This can be influenced by a range of external factors, such as a trade agreement, a war, a peace treaty, a general election, a health crisis or any other news that might affect investors’ decisions.

However, the interbank exchange rate is merely a reference figure rather than a rate at which you can actually carry out a transaction. No one, whether an individual or a company, can access this rate outside the banking system. The rate offered to other users is inevitably subject to a mark-up, the size of which depends on the individual financial intermediary.

2 – How does the margin on my trade work?

Whenever you carry out a foreign exchange transaction – whether it’s a credit card payment in a different currency, a foreign exchange transaction through your bank, or via an intermediary such as b-sharpe – a margin is applied to the exchange rate.

This refers to the fee paid to the intermediary carrying out the transaction. This margin can range from a few basis points to several per cent, depending on the amounts involved and the intermediaries involved in the transaction. It is often very difficult to obtain information about the margin applied prior to a transaction.

We can, however, estimate the margin applied in general terms. For a transaction of CHF 10,000 into euros: local banks apply a margin ranging from 1.5% to 2%, physical bureaux de change apply a margin ranging from 0.75% to 0.9%, and online intermediaries such as b-sharpe apply a margin of 0.5%.

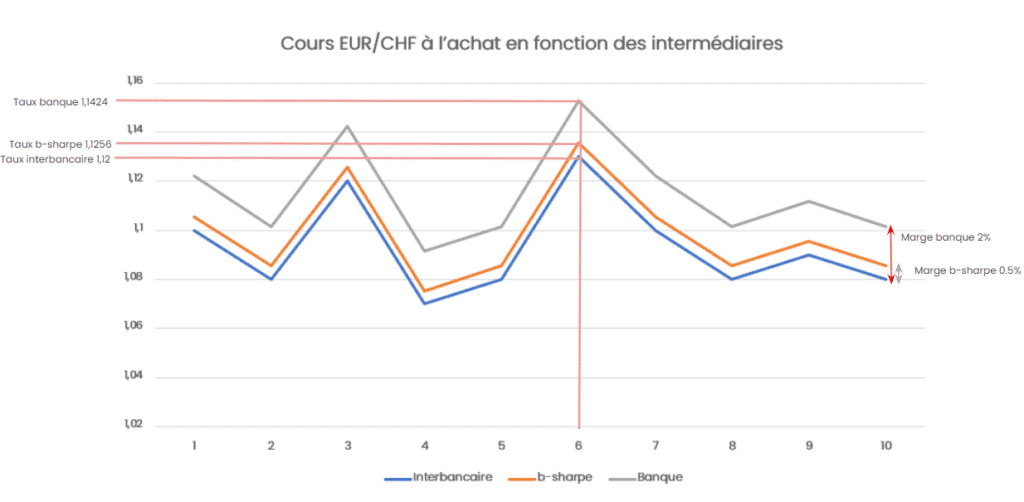

Based on these factors, the rate applied to your transaction can be calculated as follows: Intermediate rate = Interbank rate × (1 + intermediate margin), as follows:

If the interbank rate = 1.12

Bank rate = 1.12 × (1 + 0.02) = 1.12 × 1.02 = 1.1424

Spot exchange rate = 1.12 × (1 + 0.009) = 1.12 × 1.009 = 1.1301

Beta-sharpe ratio = 1.12 × (1 + 0.005) = 1.12 × 1.005 = 1.1256

As the rate changes constantly, this can be illustrated by the graph below:

3 – How much money will I receive?

To know at any given time how many euros you will receive from a Swiss franc to euro conversion, you simply need to understand the mechanism explained above. The EUR/CHF exchange rate, which is calculated by your broker and fluctuates constantly, essentially means: ‘I will have to pay XX.XX CHF to get 1 euro.’

If we take the previous example again, with an interbank rate of 1.12 and 10,000 CHF, here is the calculation to use to work out how many euros you will receive, depending on the intermediary used:

With your bank:

- Bank rate = 1.12 × (1 + 0.02) = 1.12 × 1.02 = 1.1424

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1424 = €8,753.50

Through a physical currency exchange broker:

- Spot exchange rate = 1.12 × (1 + 0.009) = 1.12 × 1.009 = 1.1301

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1301 = €8,848.77

With b-sharpe:

- Beta-sharpe ratio = 1.12 × (1 + 0.005) = 1.12 × 1.005 = 1.1256

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1256 = €8,884.15

The difference in the amount received is solely due to the margin applied to the transaction. Please note, however, that as the interbank rate fluctuates constantly, this calculation is based on a rate at a given point in time (T) that is the same for all intermediaries.

Furthermore, if the transaction is to be carried out not from CHF to € but from € to CHF, the principle remains the same; however, the interbank rate must no longer be multiplied but divided, and the amount sent must be multiplied by this rate as follows:

If the interbank rate = 1.12

B-Sharpe ratio = 1.12 / 1.005 = 1.1144

This means that for every €1 sent, you will receive 1.1144 CHF; so for €10,000, you will receive 10,000 × 1.1144 = 11,144 CHF.

You can find all our margins at: https://web.nicewit.ch/en/how-it-works/