The Japanese yen: Still a safe haven?

When the world is facing heightened geopolitical tensions, as is currently the case with the conflict in Ukraine and the Israeli-Palestinian conflict, investors turn to safe-haven assets in order to limit their losses.

A safe-haven asset is a financial instrument considered to be a stable asset, and one that may even offer upside potential during periods of financial uncertainty. Among these assets, three currencies stand out: the US dollar (USD), the Swiss franc (CHF) and the Japanese yen (JPY). But are they really always safe-haven assets?

The US dollar

The US dollar is regarded as a safe-haven asset due to the political and economic stability of the United States. Furthermore, the United States plays a dominant role in the global economy.

The Swiss franc

The Swiss franc is also seen as a stable and strong currency in times of crisis. Indeed, Switzerland is renowned for its conservative monetary policy, its highly stable financial system, and its traditional political neutrality (although this is currently being put to the test…).

The Japanese yen

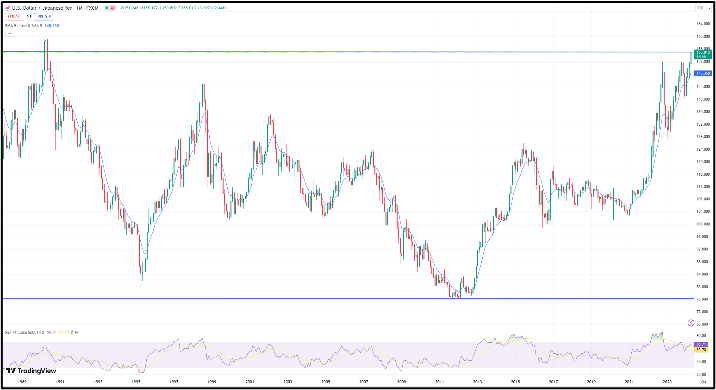

The Japanese yen is also regarded as a safe-haven currency due to Japan’s political and economic stability and the stability of its financial markets. The yen is considered a safe-haven currency because of its high liquidity in the markets. However, it should be noted that, despite its status as a safe-haven currency, the Japanese currency has currently reached its lowest level in over thirty years… Indeed, on Monday 2 April 1990, the yen was trading at 160 to the dollar, and on Wednesday 24 April 2024 it was trading at over 155 to the dollar. We can therefore no longer regard it as a safe-haven currency at present… But what are the causes of this?

Movements in the Japanese yen

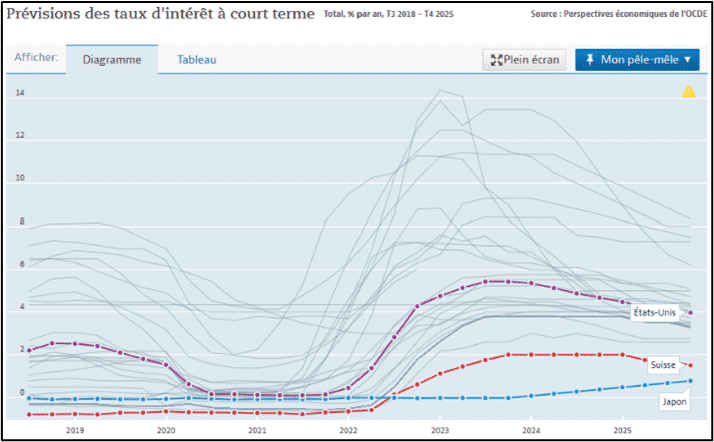

Interest rates and market dynamics are the two main factors behind this. Until March this year, short-term interest rates in Japan were negative, meaning that it was better to spend one’s money than to leave it ‘sitting idle’ in the bank. The Bank of Japan (BOJ) has abandoned this policy of negative short-term rates but remains, as shown in the OECD’s short-term interest rate forecast chart, below 0.1%, at 0.074% in the first quarter of 2024.

By way of comparison, short-term interest rates for the CHF stand at 2.003% and those for the USD at 5.357%. This rise in short-term rates has led to an increase in short positions on the yen (reaching a decade high in April 2024) and Japanese investors maintaining their liquidity abroad due to higher yields and low volatility. In other words, carry trades. These involve taking advantage of the fundamental difference in short-term interest rates between two currencies (for example, the Japanese yen at 0.074% and the US dollar at 5.375%) and exchange rate fluctuations to make a profit.

The effects of Japan’s economic policy

This significant difference between Japanese and US interest rates is due to the divergent monetary policies of the two countries. Indeed, the Bank of Japan (BOJ) pursues what is known as an ‘ultra-accommodative’ policy. This involves increasing the money supply and maintaining extremely low interest rates in order to support the Japanese economy (negative interest rates). In contrast, US monetary policy has a ‘dual mandate’ of maintaining full employment and price stability. This is why the Fed has every interest in keeping interest rates high to avoid any risk of inflation. For all these reasons, the USD/JPY exchange rate is at its highest level in over thirty years.

In conclusion, the Japanese yen is no longer regarded as a safe-haven currency, unlike the US dollar and the Swiss franc. Consequently, Japanese households, being major importers, are suffering from very high prices due to the weakness of their national currency, but can look forward to a boom in tourism given that the US dollar, the Swiss franc and even the euro are reaching record highs against the Japanese yen.

As you can see, now is the perfect time to exchange your money for yen and head to Tokyo to enjoy some sashimi and maki sushi.