And with good reason: the former, which has been hit harder by inflation but is benefiting from the post-Covid economic recovery, could well rise in value against the latter, which is seen more as a store of value…

Find out what the major banking institutions are predicting regarding the movement of the EUR/CHF exchange rate over the coming months, up until the end of 2022.

Please note: The trends described in this article are, of course, merely forecasts which, although produced by the most reputable institutions, do not engage the liability of b-sharpe.

An uncertain crisis situation

The forecasts by major banks and market experts regarding the movement of the euro-Swiss franc exchange rate – which are closely monitored by Swiss and cross-border businesses – have proved particularly difficult to make in recent months.

Whilst the global health crisis has severely disrupted the economy over the past two years, due to the numerous restrictions imposed by various European governments (ranging from the closure of certain businesses to the strictest lockdowns), the lifting of most of these restrictions at the start of the year has led to logistical bottlenecks, an inevitable consequence of a sharp rebound in demand coupled with production still hampered by health regulations and staff shortages.

Whilst economic activity and growth did indeed pick up again at the end of winter, these supply chain issues, coupled with central bank support measures, have led to widespread inflation. A generalised rise in prices inevitably impacted the foreign exchange market, but many experts at the time viewed this as merely a market blip following two years of crisis and unprecedented support from banking institutions.

However, the recent crisis stemming from the conflict between Russia and Ukraine, which has been ongoing since 24 February, has once again thrown these forecasts into disarray. With galloping inflation, particularly in fuel and food commodity prices, and an uncertain economic outlook for the two nations involved in this war, it is difficult to predict what the exchange rate between the Swiss Confederation’s two leading currencies will be by the end of 2022…

Credit Suisse’s forecasts

In early 2022, a wide-ranging study conducted by Credit Suisse among 1,100 Swiss companies provides a good indication of the outlook for the EUR/CHF exchange rate in the coming months. The study states that, of all the companies surveyed, 80% purchase some of their inputs in the single currency, whilst nearly 70% sell their products or services in Swiss francs.

On this occasion, the economic stakeholders surveyed, as well as Credit Suisse’s foreign exchange strategists, all predict an end to the downward trend in the EUR/CHF exchange rate that has been in place since 2017. They therefore anticipate a slight appreciation of the euro against the Swiss franc: businesses are forecasting an exchange rate of 1.08 by the end of 2022 (compared with 1.05 by the end of 2021), whilst Credit Suisse takes this trend even further, forecasting a rate of 1.10.

Why is the euro expected to appreciate against the Swiss franc over the coming months? With inflation more pronounced in the eurozone than in Switzerland, it seems likely that the European Central Bank (ECB) will have to raise interest rates sooner than the Swiss National Bank (SNB).

At the same time, the use of the Swiss franc as a store of value – which contributed to its appreciation during the toughest months of the Covid crisis – is likely to decline, logically leading to a slight depreciation of the Swiss currency. Finally, as has been demonstrated in the past, periods of economic recovery tend to favour the euro.

Update: Against all expectations, the SNB finally decided to raise its interest rates on 16 June (the first such move since September 2007), bringing them up from -0.75% to -0.25%, in order to prevent inflation from spreading.

At the same time, the use of the Swiss franc as a store of value – which contributed to its appreciation during the toughest months of the Covid crisis – is likely to decline, logically leading to a slight depreciation of the Swiss currency. Finally, as has been demonstrated in the past, periods of economic recovery tend to favour the euro.

The war in Ukraine and inflation are at the heart of market expectations

The blind spot in these forecasts is, of course, the crisis in Ukraine. Whilst Credit Suisse had already announced at the start of the year that inflation would be one of the three key factors likely to influence the exchange rate between the euro and the Swiss franc, the bank could not have anticipated an even sharper rise in prices caused by an armed conflict in Europe!

Whilst the Swiss economy is clearly better protected against this phenomenon than the eurozone, it nevertheless called into question the SNB’s forecasts last March: the SNB had anticipated an inflation rate of +2.1% for 2022, followed by just +0.9% in 2023, whereas it had already reached +2.5% in April. There is no doubt that this is a figure to be monitored closely in order to forecast the trend of the EUR/CHF pair.

At the same time, the European Commission announced last May that it had revised its growth forecast downwards (reducing it by 1.3 percentage points to 2.7% for 2022) and its inflation forecast upwards (by 3.5 percentage points to 6.8% for the year) for the eurozone as a whole.

These trends are entirely attributable to the war in Ukraine and cast a somewhat different light on the forecasts made in the survey conducted by Credit Suisse earlier this year. Indeed, slower economic growth in Europe and soaring inflation, particularly in energy prices, could limit the euro’s appreciation against the Swiss franc.

The health crisis, supply chain issues, inflation and now the Russia-Ukraine conflict… There is no doubt that the last two years have been turbulent on the markets! Whilst the major banks are forecasting a slight appreciation of the euro against the Swiss franc over the coming months, it is difficult to say for certain in such a context.

In any case, all banking institutions encourage businesses to hedge against currency risk in the face of market volatility. To do so, please do not hesitate to contact b-sharpe for their specialist services!

The euro: has Brexit strengthened the single currency?Having risen by more than 10% against the US dollar over the past 12 months, the euro (EUR) has paused for breath at the start of 2021, much to the delight of eurozone exporters, who were put under severe strain last year.

Despite a slight fall against the pound sterling (GBP) following the free trade agreement signed between London and Brussels, the single currency has, all things considered, held up rather well in the face of Brexit so far.

Nevertheless, whilst it is tempting to imagine that the UK’s departure from the European Union will have only a limited impact on the single currency in the coming months, given that it is not part of the eurozone, the situation is not quite so straightforward, and the close trade links across the Channel could well come into play in the medium to long term. Here’s why.

A limited direct impact, but very real economic consequences

At an institutional level, Brexit entails the United Kingdom’s withdrawal from the European System of Central Banks (ESCB), which comprises the European Central Bank (ECB), the central banks of the nineteen eurozone member states, and the nine central banks of EU member states that do not belong to the single currency area – the Bank of England (BoE) being part of the latter group.

Nevertheless, whilst the United Kingdom had obviously never joined the eurozone, it was also not part of the European exchange rate mechanism linking the national currencies of member states (outside the eurozone) to the single currency. For this reason, the implementation of Brexit, followed by the signing of the trade agreement between the EU and its former member state on 24 December last year, had only a limited direct impact on the value of the euro.

Brexit, however, has very real consequences for the European economy, which are affecting – and are likely to continue to affect – the value of its currency. To name just one example, EU member states now face a shortfall of nearly €60 billion in their budget forecasts by 2027!

The balance of power is generally in the euro’s favour

Since the referendum on the United Kingdom’s membership of the European Union on 23 June 2016, UK financial markets have, on average, underperformed those of the eurozone (which was not the case prior to the vote). For example, the MSCI UK Index has fallen by 8% since the referendum, whilst the MSCI Eurozone Index has risen by nearly 32%.

Furthermore, the pound sterling, which was worth €1.3089 at the time of the Brexit vote, is now worth just €1.1285. Despite the many uncertainties surrounding the departure of a key trading partner, the single currency has so far retained its strength and stability.

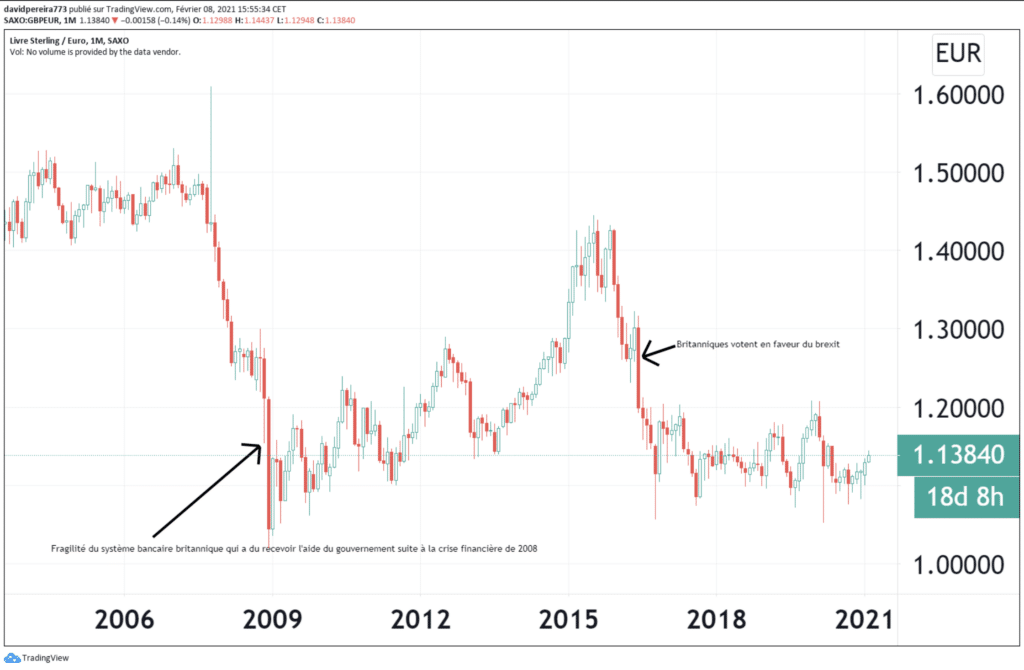

Movements in the GBP/EUR exchange rate

The GBP/EUR exchange rate has been highly volatile over the past two decades. The most dramatic fall occurred during the 2008 financial crisis, when the pound sterling lost almost 40% against the euro, falling from 1.60 to 1.02 by the end of December 2008 – a level that remains, for the time being, the closest the currency has come to parity. Following this slump, between 2009 and 2014, the pound sterling regained strength and traded within a range of 1.10 to 1.25. The year 2015 saw an uptrend, with the pair trading around 1.35–1.40. A further collapse (-25%) in 2016 (following the British vote in favour of Brexit) reversed the previous year’s upward trend, with the rate falling back to 1.10; for the past five years, the pair has fluctuated between strong support at 1.08 and significant resistance at 1.20.

In terms of both stock markets and monetary policy, the advantage (or the lesser of two evils) seems to lie with the eurozone so far. But what about the economic picture?

Whilst it is still too early to quantify precisely the economic consequences of Brexit for the eurozone, it is nevertheless possible to describe the movements of assets observed between the two economic areas.

Indeed, the Governor of the Banque de France, François Villeroy de Galhau, announced on Tuesday 19 January that further relocations were planned for 2021, following on from the transfer of some 2,500 jobs and €170 billion in assets from London to France at the end of 2020.

For its part, the German Bundesbank reported that nearly €400 billion in assets had been transferred, to which a further €100 billion from Morgan Stanley is expected to be added shortly.

This wave of companies relocating from central London to Europe’s major financial centres presents a golden opportunity for the EU to strengthen its own infrastructure. These capital movements are in line with the ECB’s 2019 announcement, which estimated that 24 banks and nearly €1.3 trillion in assets would eventually move from London to the eurozone.