BEN, SHARE, OUR: International payment options

When making an international payment, you can choose how the fees are allocated. In this article, we explain the difference between the three possible arrangements: whether the sender covers all the fees, the fees are shared, or they are charged to the recipient.

Which payments are affected?

This article will examine the payment framework applicable to all international financial transactions outside the SEPA area. Indeed, this framework entails a cost structure that is directly determined by the directives and specific characteristics of this type of transaction.

These various schemes therefore apply to all transfers outside the SEPA framework, including express payments in euros, which by definition fall outside the SEPA framework.

Why are there charges on international transfers?

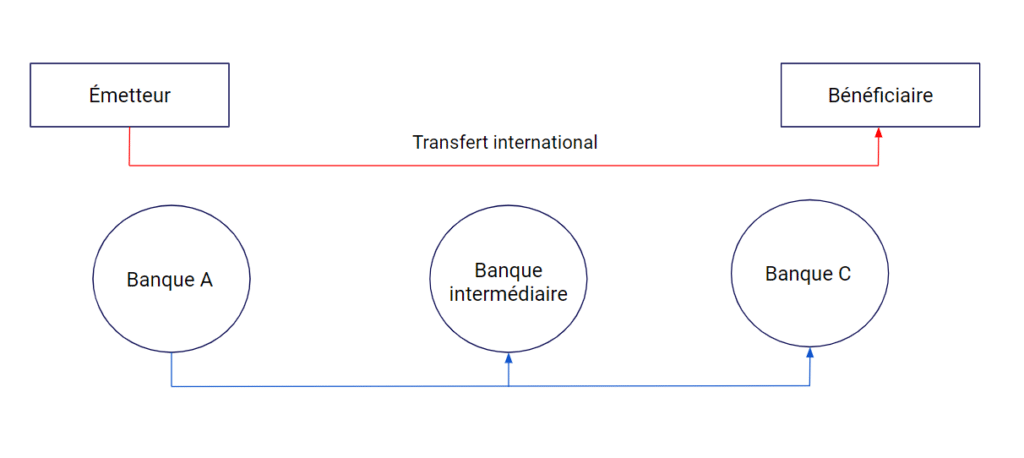

A banking transaction involves more than just transferring funds from Bank A to Bank B; it is a secure and reliable transfer of information between two private entities, often operating in different countries, which may require the involvement of several other entities in order to reach its destination.

As part of the process of setting up this payment, there are fees associated with the processing carried out by the financial institutions involved in the transaction. These fees can be substantial and must be taken into account before any payment is made.

These charges generally consist of administration and processing fees and, unfortunately, can very rarely be predicted in advance of a transaction. To manage these charges, banks and financial institutions have introduced standardised payment and cost schemes. These schemes determine whether the sender or the recipient is responsible for the transfer charges.

These administration and payment fees usually range from a few francs to several dozen francs for a transfer to the United States, for example.

There are currently three main fee structures: OUR, BEN and SHA. Each of these three structures has its own specific features and advantages.

The three cost models:

To explain the conditions for each of these three options, we will refer back to the diagram at the top of the page.

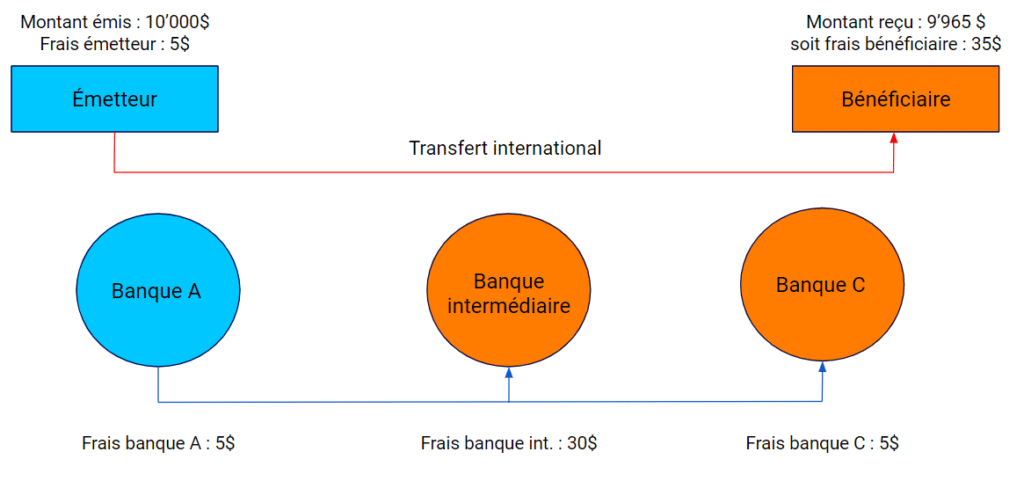

SHA: Share or cost-sharing

This is the default scheme used when processing a financial transaction. This scheme allocates the charges between the issuer and the beneficiary. The allocation is as follows:

- The costs relating to the issuer’s bank (Bank A) are to be borne by the issuer.

- Any charges relating to the intermediary bank and the beneficiary’s bank (Bank C) are to be borne by the beneficiary.

Please note that when making a payment using this method, the recipient is likely to receive a lower amount than the amount you have sent. It is therefore important to specify the method used when settling the invoice.

This is particularly important when paying an invoice to China or the United States, as intermediary banks will inevitably charge for their services.

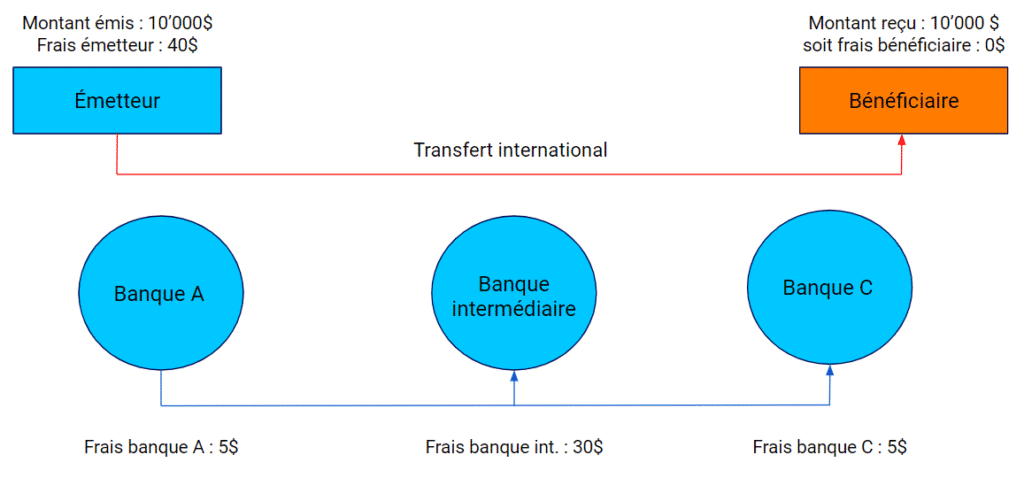

OUR: Our or costs to be borne by the issuer

This method is much more specific and less common, but it ensures that the recipient receives the full amount sent by the sender. In this case, the sender covers all the costs associated with the transaction; consequently, the recipient does not have to pay anything and receives the full amount sent.

As the costs are unpredictable, financial institutions tend to charge a flat fee to cover all expenses. This usually costs around thirty francs and is specifically intended for business use.

As this form is not used by default, please do not hesitate to ask your financial advisor if it is the one you need.

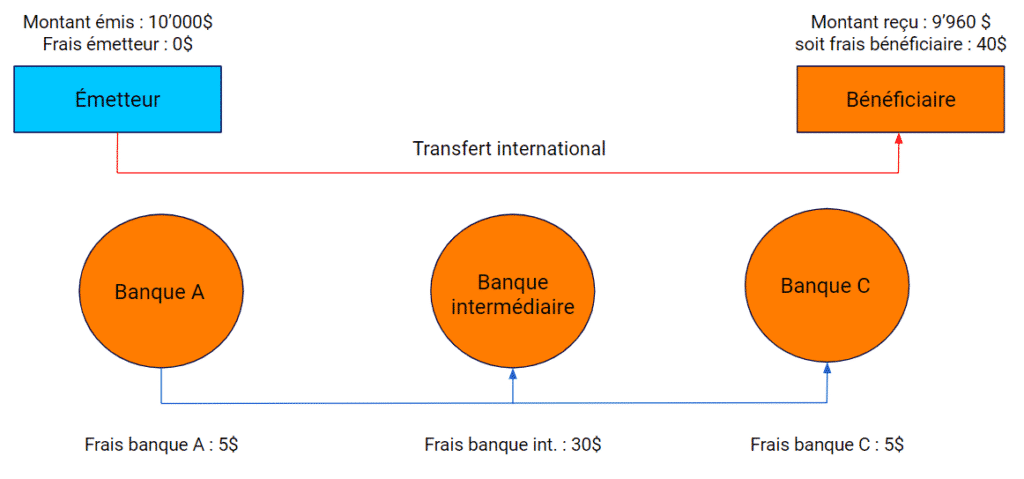

BEN: Beneficiary or costs to be borne by the beneficiary

This method is rarely used; it is often costly for the beneficiary and therefore does not provide a solution to the issues surrounding the payment of an invoice. However, it can be useful when it is impossible to determine the cost of a transaction with certainty, or in the context of certain contracts.

In this scenario, all costs associated with the transaction are borne by the recipient. Consequently, the sender knows exactly how much will be debited from their account, whereas the recipient can be certain that they will receive an amount lower than the amount sent. This is useful when no agreement has been signed and you wish to pay a specific amount, regardless of the amount received by the recipient.

What about b-sharpe, then?

As part of our service enabling you to pay your international suppliers directly, b-sharpe is able to offer you these three pricing options.

Like other financial institutions, we use the SHA scheme by default and free of charge.

At your request, and when processing your invoice payment, we can use the OUR scheme and therefore cover the full cost of the transfer. This scheme costs CHF 28.

Although the BEN scheme is less commonly used, it remains available and is completely free of charge.

Conclusion

The cost structure is therefore a key factor in the signing and management of a commercial contract involving international financial transactions. Each of these three solutions is sound and has its own advantages and disadvantages. As part of our business, we offer these three methods depending on your needs and the constraints governing your international contracts. Please do not hesitate to contact us for advice on the best solution to use for your transactions. Our teams will be happy to provide you with the necessary guidance to ensure the successful completion of your transaction.

On the same topic