The euro: has Brexit strengthened the single currency?

Having risen by more than 10% against the US dollar over the past 12 months, the euro (EUR) has paused for breath at the start of 2021, much to the delight of eurozone exporters, who were put under severe strain last year. Despite a slight fall against the pound sterling (GBP) following the free trade […]

Having risen by more than 10% against the US dollar over the past 12 months, the euro (EUR) has paused for breath at the start of 2021, much to the delight of eurozone exporters, who were put under severe strain last year.

Despite a slight fall against the pound sterling (GBP) following the free trade agreement signed between London and Brussels, the single currency has, all things considered, held up rather well in the face of Brexit so far.

Nevertheless, whilst it is tempting to imagine that the UK’s departure from the European Union will have only a limited impact on the single currency in the coming months, given that it is not part of the eurozone, the situation is not quite so straightforward, and the close trade links across the Channel could well come into play in the medium to long term. Here’s why.

A limited direct impact, but very real economic consequences

At an institutional level, Brexit entails the United Kingdom’s withdrawal from the European System of Central Banks (ESCB), which comprises the European Central Bank (ECB), the central banks of the nineteen eurozone member states, and the nine central banks of EU member states that do not belong to the single currency area – the Bank of England (BoE) being part of the latter group.

Nevertheless, whilst the United Kingdom had obviously never joined the eurozone, it was also not part of the European exchange rate mechanism linking the national currencies of member states (outside the eurozone) to the single currency. For this reason, the implementation of Brexit, followed by the signing of the trade agreement between the EU and its former member state on 24 December last year, had only a limited direct impact on the value of the euro.

Brexit, however, has very real consequences for the European economy, which are affecting – and are likely to continue to affect – the value of its currency. To name just one example, EU member states now face a shortfall of nearly €60 billion in their budget forecasts by 2027!

The balance of power is generally in the euro’s favour

Since the referendum on the United Kingdom’s membership of the European Union on 23 June 2016, UK financial markets have, on average, underperformed those of the eurozone (which was not the case prior to the vote). For example, the MSCI UK Index has fallen by 8% since the referendum, whilst the MSCI Eurozone Index has risen by nearly 32%.

Furthermore, the pound sterling, which was worth €1.3089 at the time of the Brexit vote, is now worth just €1.1285. Despite the many uncertainties surrounding the departure of a key trading partner, the single currency has so far retained its strength and stability.

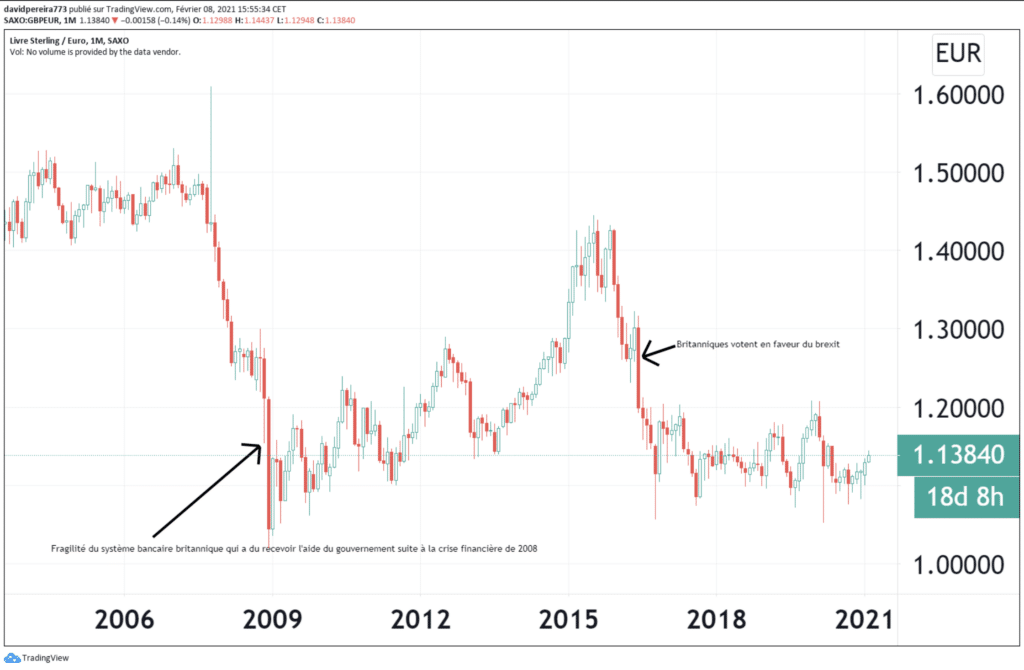

Movements in the GBP/EUR exchange rate

The GBP/EUR exchange rate has been highly volatile over the past two decades. The most dramatic fall occurred during the 2008 financial crisis, when the pound sterling lost almost 40% against the euro, falling from 1.60 to 1.02 by the end of December 2008 – a level that remains, for the time being, the closest the currency has come to parity. Following this slump, between 2009 and 2014, the pound sterling regained strength and traded within a range of 1.10 to 1.25. The year 2015 saw an uptrend, with the pair trading around 1.35–1.40. A further collapse (-25%) in 2016 (following the British vote in favour of Brexit) reversed the previous year’s upward trend, with the rate falling back to 1.10; for the past five years, the pair has fluctuated between strong support at 1.08 and significant resistance at 1.20.

In terms of both stock markets and monetary policy, the advantage (or the lesser of two evils) seems to lie with the eurozone so far. But what about the economic picture?

Whilst it is still too early to quantify precisely the economic consequences of Brexit for the eurozone, it is nevertheless possible to describe the movements of assets observed between the two economic areas.

Indeed, the Governor of the Banque de France, François Villeroy de Galhau, announced on Tuesday 19 January that further relocations were planned for 2021, following on from the transfer of some 2,500 jobs and €170 billion in assets from London to France at the end of 2020.

For its part, the German Bundesbank reported that nearly €400 billion in assets had been transferred, to which a further €100 billion from Morgan Stanley is expected to be added shortly.

This wave of companies relocating from central London to Europe’s major financial centres presents a golden opportunity for the EU to strengthen its own infrastructure. These capital movements are in line with the ECB’s 2019 announcement, which estimated that 24 banks and nearly €1.3 trillion in assets would eventually move from London to the eurozone.